In the intricate landscape of personal finance and business, few concepts carry as much weight yet remain as frequently misunderstood as depreciation. When you make a significant purchase, be it equipment for your enterprise or a high-value personal item, its initial cost is merely the starting point. Over time, that asset’s value will inevitably shift, and how this change is recorded can profoundly impact your financial standing, tax obligations, and future investment strategies.

Many often simplify depreciation to just the ‘wearing out’ of an item or a straightforward loss of market value. While this perspective captures a part of the truth, the accounting and financial implications extend far deeper. Grasping these complexities isn’t exclusive to seasoned financial professionals; it’s an indispensable skill for anyone aiming to make astute decisions about their assets, manage finances efficiently, and proactively avoid potential financial pitfalls.

This comprehensive guide is designed to clarify the concept of depreciation, distilling it into 12 essential principles that every financially savvy individual and business owner should internalize for 2025 and beyond. We will explore not only what depreciation entails but also its diverse calculation methods, its profound effects on financial statements, and its intricate relationship with your tax responsibilities. By mastering this knowledge, you will be empowered to accurately assess the true economic cost of asset ownership, strategically plan for future expenditures, and ultimately, make more informed and robust financial choices in our dynamic economic environment.

1. Understanding Depreciation: More Than Just Value Loss

In common parlance, depreciation typically refers to an asset’s straightforward decline in market value. This is the difference between its original purchase price and its current worth. For instance, a new vehicle often drops significantly in value upon leaving the dealership. This immediate reduction in fair value is a visible form of depreciation, reflecting diminished worth due to usage, wear and tear, or simply time. It provides a direct measure of what someone would pay for that item today versus its brand-new price.

However, the accounting definition of depreciation encompasses a critical second dimension: the systematic allocation of an asset’s initial cost over the periods it’s expected to generate economic benefits. This means depreciation isn’t merely observing a loss; it’s a structured method to spread out a long-lived asset’s capital expenditure across its “useful life.” Instead of expensing the entire acquisition cost in one period, a portion is gradually recognized over many periods.

This cost allocation is central to the “matching principle” in accounting, ensuring expenses are recognized in the same period as the revenues they help produce. For example, factory machinery contributes to production over several years, so its cost is expensed proportionally over those years. Understanding this dual nature—both the actual decline in fair value and the systematic expensing of cost—is foundational to appreciating depreciation’s true impact on financial health and reporting.

Read more about: Decoding the Drive: Why Your Luxury Sedan’s Value Might Vanish Faster Than a Business Truck’s Tax Benefits

2. The Four Pillars of Depreciation Calculation

For those managing valuable assets, mastering depreciation calculation is indispensable. This isn’t arbitrary; it rests upon four fundamental criteria, ensuring a consistent and accurate approach to valuing and expensing long-term assets. These pillars are critical inputs for any depreciation method, acting as the bedrock for sound financial decision-making and reporting. Grasping each element clarifies an asset’s true cost over its lifespan.

The first criterion is the “Cost of the asset,” extending beyond the sticker price. It includes all expenses to acquire and prepare the asset for its intended operational use, such as purchase price, shipping, and installation. This comprehensive sum establishes the “depreciable basis”—the total amount to be systematically allocated. An accurate initial cost is vital for all subsequent financial calculations.

Secondly, the “Expected salvage value,” or residual value, is the estimated worth of the asset at the end of its projected useful life. Depreciation only applies to the portion of the asset’s cost expected to be consumed, so this recoverable value is subtracted from the initial cost. Concurrently, the “Estimated useful life of the asset” determines the period of expected economic benefit, differing from physical lifespan. This estimation relies on factors like industry benchmarks and anticipated obsolescence.

Finally, selecting “A method of apportioning the cost over such life” completes the framework. This specific formula distributes the depreciable cost over the asset’s estimated useful life, using methods like straight-line or diminishing balance. The chosen method significantly impacts the timing and magnitude of depreciation expenses, directly affecting net income and tax obligations, making its selection a key financial decision.

3. The Critical Role of Salvage Value

Salvage value, also known as residual value, is a critical detail significantly impacting depreciation calculations and financial reporting. It represents the estimated worth of an asset at the conclusion of its “useful life”—the point it’s expected to be retired or sold. Accurately estimating this value isn’t just an accounting formality; it’s a practical consideration influencing the total depreciation expense recognized over an asset’s lifetime.

The fundamental principle is that an asset is only depreciated down to its expected residual worth. If a machine is anticipated to fetch $2,000 at the end of its useful life, only the portion of its initial cost *above* $2,000 will be allocated as depreciation expense. This $2,000 is considered a recoverable amount, not a cost consumed by the asset’s operation. Thus, a higher estimated salvage value leads to a lower total depreciable amount and smaller annual depreciation expense.

Salvage value can sometimes be zero, implying no market value at the end of its useful life. The context notes it can even be “negative due to costs required to retire it,” though for depreciation purposes, it’s generally not calculated below zero. Predicting this future value accurately is challenging, as economic conditions, technology, and market demand can all shift, making precise forecasts difficult.

From a financial planning perspective, a robust estimate of salvage value offers multiple benefits. It provides a more realistic picture of an asset’s true economic consumption, informing future capital budgeting. Consistently high salvage values might signal a favorable total cost of ownership. Conversely, overestimating can understate depreciation, potentially inflating reported profits. Treating salvage value as a critical input, not an afterthought, is a hallmark of diligent financial management.

Read more about: Unlocking the Mystery: Why Your Car Key Fob Replacement Can Cost Hundreds of Dollars

4. Beyond the Obvious: Impairment Charges

While depreciation systematically allocates an asset’s cost over its useful life, what happens when its value unexpectedly plummets? This scenario necessitates “impairment charges,” a distinct, often non-recurring expense profoundly impacting financial statements. Unlike predictable depreciation, impairment occurs when an asset’s fair value abruptly declines below its “carrying amount” on the balance sheet. It’s an accounting mechanism reflecting a sudden, substantial loss in economic worth.

The need for an impairment charge arises from unforeseen events or drastic changes indicating an asset may not recover its carrying amount through future use or sale. Key triggers include a “Large amount of decrease in fair value,” perhaps from market shifts or obsolescence; “A change of manner in which the asset is used,” altering its economic potential; or “Accumulation of costs that are not originally expected to acquire or construct an asset,” inflating its book value. A “projection of incurring losses associated with the particular asset” also prompts reassessment.

When these indicators emerge, companies perform a “recoverability test” to confirm impairment. This involves estimating the asset’s future cash flow from both ongoing use and eventual disposition. If the “sum of the expected cash flow is less than the carrying amount of the asset, the asset is considered impaired.” This prevents assets from being overstated on the balance sheet. The asset’s carrying amount is then reduced to its fair value, with the difference recorded as an impairment loss on the income statement.

For astute financial observers, impairment charges are significant red flags. They often point to deeper issues like struggling product lines, industry shifts, or poor asset utilization. While typically “nonrecurring,” their impact can be substantial, leading to lower reported profits and a reduced asset base. Understanding impairment goes beyond basic depreciation; it involves recognizing sudden, sharp downturns that affect asset value and, consequently, financial stability, providing crucial insights for informed decision-making.

5. Depreciation’s Tricky Dance with Cash Flow

One of depreciation’s most counterintuitive aspects is its relationship with cash flow. There’s a common misconception that it represents an actual outflow of cash. However, as the context explicitly states, “Depreciation expense does not require a current outlay of cash.” This fundamental truth establishes depreciation as a “non-cash expense,” a crucial distinction when interpreting financial performance and liquidity. The initial cash outflow occurs when the asset is purchased; annual depreciation is merely an accounting allocation of that past expenditure.

Each year, a portion of the asset’s initial cost is recognized as an expense on the income statement, reducing reported profits. Crucially, no new cash is spent when this annual depreciation expense is recorded; the funds were already disbursed during acquisition. Despite not being a direct cash expense, depreciation plays a vital indirect role in cash flow analysis. On a statement of cash flows, it’s typically added back to net income when calculating cash flow from operating activities, as net income has already been reduced by this non-cash item.

This adjustment clarifies actual cash generated by core operations. The context explains that “provided the enterprise is operating… depreciation is a source of cash in a statement of cash flows, which generally offsets the cash cost of acquiring new assets required to continue operations when existing assets reach the end of their useful lives.” For consumers and small business owners, recognizing depreciation as a non-cash expense is empowering. It means an asset losing book value doesn’t directly translate to money leaving your wallet each period, aiding accurate budgeting and cash flow forecasting.

6. Unpacking Accumulated Depreciation

When reviewing a company’s balance sheet, you will invariably encounter “accumulated depreciation.” This account is indispensable for comprehending an entity’s true financial standing, particularly concerning its long-term tangible assets. Categorized as a “contra account,” its balance always opposes the normal balance of the related asset account. While assets usually carry debit balances, accumulated depreciation holds a credit balance, effectively reducing the book value of associated assets.

The purpose of accumulated depreciation is two-fold. First, it plays a critical role in “preserving the historical cost of assets on the balance sheet.” Instead of directly reducing the original acquisition cost of, say, machinery, it functions as a separate ledger. This ledger meticulously tallies all depreciation expense recorded for those assets since their initial purchase. This approach allows financial statements to simultaneously display both historical cost and current depreciated book value (original cost minus accumulated depreciation), offering a more comprehensive historical context.

Each period, as depreciation expense is recognized on the income statement, a corresponding entry increases the accumulated depreciation account on the balance sheet. Over time, this account grows, serving as a cumulative record of the asset’s economic consumption. This explains why “values of the fixed assets stated on the balance sheet will decline, even if the business has not invested in or disposed of any assets.” Understanding this offers vital insights into the age and remaining economic value of an asset base, informing strategic decisions about replacement and budgeting.

Read more about: The 15 Cars Owners Regret Most: Why Their Value Dives Faster Than You Think

7. Straight-Line Depreciation: The Foundation of Allocation

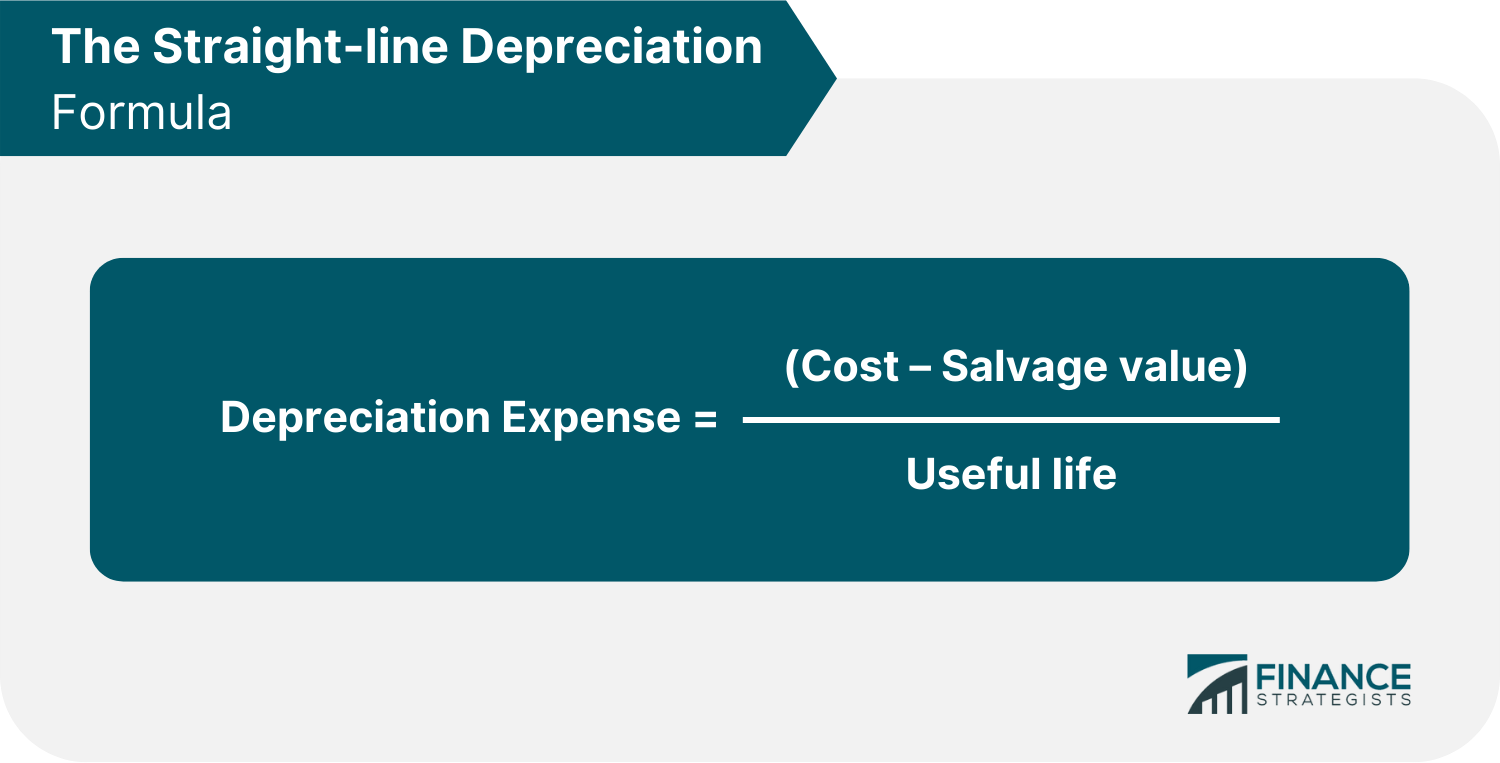

Transitioning from the foundational concepts of depreciation, we now delve into the various methodologies used to calculate this crucial financial allocation. Among them, the straight-line depreciation method stands out as the most straightforward and widely adopted approach. Its appeal lies in its simplicity: it systematically distributes the total depreciable cost of an asset evenly over its entire useful life, ensuring a consistent expense recognition each period. This method makes financial planning and forecasting considerably easier for businesses and individuals alike, offering a predictable decline in an asset’s book value.

The calculation for straight-line depreciation is refreshingly direct. As outlined in financial principles, the “annual depreciation expense” is determined by taking the “cost of fixed asset” minus its “residual value” (or salvage value), and then dividing this figure by the asset’s “useful life of asset (years).” For instance, consider a vehicle purchased for $17,000 with an expected salvage value of $2,000 after 5 years of useful life. Using the straight-line method, the annual depreciation would be ($17,000 – $2,000) / 5 years, which equates to a predictable $3,000 per year.

Each year, this $3,000 is recognized as depreciation expense, steadily reducing the asset’s “book value”—which is the original cost minus accumulated depreciation. Starting with an initial book value of $17,000, after one year it becomes $14,000, then $11,000, and so on, until it reaches its $2,000 salvage value at the end of its fifth year. This systematic reduction provides a clear snapshot of the asset’s decreasing value on the balance sheet, reflecting its consumption over time. It offers a transparent way to track an asset’s declining worth.

Moreover, understanding the straight-line method’s implications is essential for tax planning. If an asset is sold for more than its depreciated book value, the excess is considered a gain and may be subject to “depreciation recapture” as ordinary income by tax authorities. Conversely, selling below book value can result in a capital loss, which is typically tax-deductible. These nuances highlight why aligning depreciation strategies with tax regulations is crucial, as differences can create timing discrepancies in reported profits.

8. Diminishing Balance Method: Accelerating Your Write-Offs

While the straight-line method offers consistency, some assets lose a greater proportion of their value, or are more productive, in their earlier years. For such scenarios, accelerated depreciation methods like the “double-declining-balance method,” also known as the reducing balance method, provide a more aggressive approach to expense recognition. This method front-loads depreciation, allowing businesses to claim larger deductions in the initial years of an asset’s useful life, which can significantly impact early financial statements and tax obligations.

The core principle of the diminishing balance method is to apply a fixed depreciation rate to the asset’s *non-depreciated book value* each year, rather than its original cost. Crucially, while salvage value is a consideration in overall depreciation, it is not subtracted from the cost *before* calculating annual depreciation with this method. Instead, the asset’s book value is simply never allowed to fall below its estimated salvage value, acting as a floor. This ensures that the asset is not depreciated beyond its expected residual worth.

Consider an asset with an original cost of $1,000 and a 40% depreciation rate. In the first year, the depreciation expense would be $400 (40% of $1,000), reducing the book value to $600. In the second year, the 40% rate is applied to the *new* book value of $600, resulting in an expense of $240. This pattern continues, with the annual depreciation expense decreasing over time, reflecting the accelerated nature of the method. The book value steadily declines, but it will halt once it reaches the specified salvage value.

This method often provides a “better representation of how vehicles depreciate” and can “more accurately match cost with benefit from asset use.” For instance, a delivery truck experiences its most intense usage and significant wear and tear in its initial years, generating more revenue. The diminishing balance method reflects this by allocating more of its cost to those high-productivity periods. Additionally, some strategies involve converting from the declining-balance method to straight-line depreciation at a midpoint in the asset’s life to ensure full depreciation if the declining balance alone wouldn’t reach the salvage value by the end of the useful life, offering flexibility in financial reporting.

9. Activity-Based Depreciation: Linking Cost to Usage (Units-of-Production)

Beyond time-based depreciation, activity-based methods offer a highly precise way to match an asset’s expense to its actual utilization. Unlike straight-line or diminishing balance, which allocate costs based on the passage of time, activity-based depreciation ties the expense directly to the “level of activity (or use) of the asset.” This could be measured in “miles driven for a vehicle, or a cycle count for a machine,” making it particularly relevant for assets whose economic benefit is primarily derived from their output or operational intensity rather than just their age.

One prominent example of this approach is the units-of-production method. This method calculates a depreciation rate per unit of activity, which is then multiplied by the actual units produced or utilized in a given period to determine the depreciation expense. For instance, if an asset has an original cost of $70,000, an expected salvage value of $10,000, and is estimated to produce 6,000 units over its lifetime, the depreciation per unit would be ($70,000 – $10,000) / 6,000 units, resulting in a rate of $10 per unit.

Once the per-unit depreciation cost is established, the annual depreciation expense becomes directly proportional to the asset’s actual output. If, in one year, the asset produces 1,000 units, the depreciation expense for that year would be $10,000 (1,000 units x $10/unit). If the next year it produces 1,100 units, the expense would be $11,000. This ensures that “greater deductions for depreciation” are taken “in years when the asset is heavily used,” providing a highly accurate reflection of the asset’s economic consumption.

This method is invaluable for businesses that experience fluctuating asset usage, as it avoids over-depreciating an underused asset or under-depreciating one that is operating at maximum capacity. By directly linking the expense to the asset’s output, companies gain a clearer picture of the true cost of production and can make more informed decisions about asset utilization and replacement. It’s an empowering tool for financial managers seeking precision in their cost accounting.

10. Sum-of-Years-Digits Method: A Deeper Dive into Accelerated Expense

Another powerful accelerated depreciation technique, often yielding even faster write-offs than the straight-line method, is the Sum-of-Years-Digits (SYD) method. This approach is built on the premise that assets are generally “more productive when they are new and their productivity decreases as they become old.” Consequently, SYD allows for higher depreciation expenses in the earlier years of an asset’s life, aligning costs more closely with the period of greatest economic benefit.

To implement the SYD method, you first need to calculate the “sum of the years’ digits.” For an asset with a 5-year useful life, the digits are 5, 4, 3, 2, and 1. Summing these gives 15. Alternatively, a shortcut formula, (n² + n) / 2 where ‘n’ is the useful life, can be used; for 5 years, (5² + 5) / 2 also equals 15. This sum then becomes the denominator in a series of fractions used to determine the annual depreciation, with the numerator being the remaining useful life for each year.

Now, let’s apply this to an example: an asset with an original cost of $1,000, a 5-year useful life, and a $100 salvage value. The “depreciable base” (cost minus salvage value) is $900. In the first year, the depreciation rate is 5/15, resulting in an expense of $300 ($900 x 5/15). In the second year, the rate drops to 4/15, yielding an expense of $240. This pattern continues, with the highest depreciation occurring in the first year and systematically declining as the asset ages.

This methodical reduction in annual depreciation expense means a significant portion of the asset’s cost is recovered earlier, which can be advantageous for tax purposes and cash flow management, particularly for businesses seeking to minimize taxable income in the early stages of an asset’s operation. By understanding and strategically applying methods like SYD, financial decision-makers can optimize their asset management and financial reporting, gaining greater control over their economic outlook.

11. Tax Depreciation: Unlocking Cost Recovery and Capital Allowances

Moving beyond accounting depreciation, the concept takes on another critical dimension in the realm of taxation. “Most income tax systems allow a tax deduction for recovery of the cost of assets used in a business or for the production of income.” This isn’t merely an accounting entry; it’s a vital mechanism for businesses and individuals to reduce their taxable income, effectively recovering the capital they’ve invested in long-term assets. Understanding tax depreciation is therefore paramount for effective financial planning and maximizing after-tax profits.

A common system for tax depreciation is known as “capital allowances,” particularly in regions like the United Kingdom and Canada. Under this system, “a fixed percentage of the cost of depreciable assets” is permitted to be deducted each year. For instance, “Canada’s Capital Cost Allowance” specifies “fixed percentages of assets within a class or type of asset.” These percentages, defined by tax laws and regulations, are multiplied by the asset’s tax basis to determine the allowable deduction, directly impacting a taxpayer’s bottom line.

The application of these allowances can vary. Calculations “may be based on the total set of assets, on sets or pools by year (vintage pools) or pools by classes of assets.” This flexibility allows tax systems to tailor depreciation rules to different industries and asset types, ensuring fairness and encouraging investment. For a financially savvy individual or business, grasping these rules translates into real savings, as legitimate deductions reduce the overall tax burden and free up capital for other ventures or reinvestment.

However, it’s important to note that tax depreciation rules often differ from financial accounting depreciation. While financial depreciation aims to match expenses to revenues, tax depreciation primarily serves as a fiscal tool for encouraging investment and simplifying compliance. This distinction can create “timing differences” in financial reporting but is a key lever for managing tax liabilities and optimizing cash flow from a tax perspective. Strategic use of capital allowances is a cornerstone of prudent financial management.

12. Navigating Tax Authority Guidelines and Finding Support.

The complexities of tax depreciation extend beyond mere calculation; they involve navigating specific guidelines set by tax authorities regarding “tax lives and methods.” Many systems, like that of the United States Internal Revenue Service (IRS) and the Canada Revenue Agency, “specify lives based on classes of property defined by the tax authority,” offering detailed guidance on how different asset types should be depreciated for tax purposes. These guidelines are crucial, as non-compliance can lead to penalties or disallowed deductions.

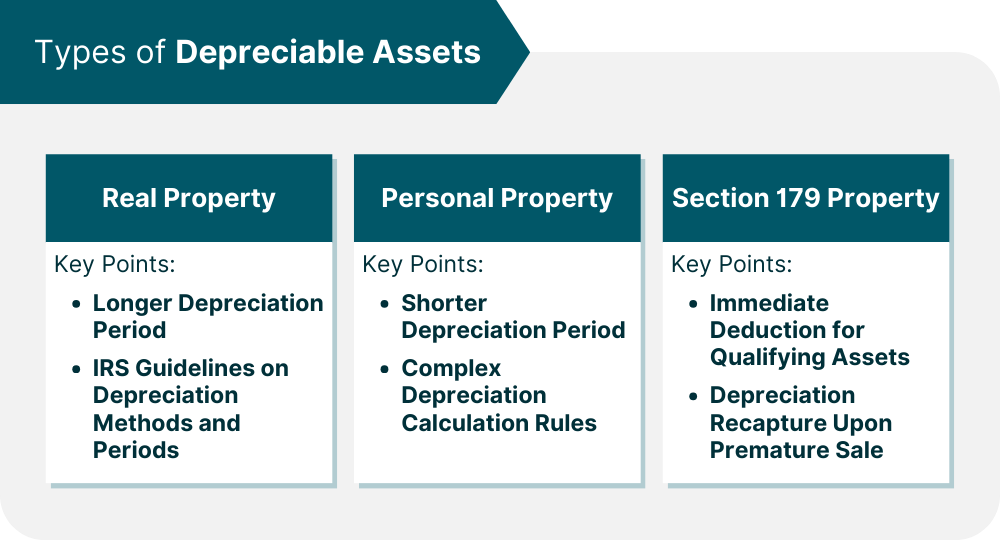

These authoritative bodies publish comprehensive tables of asset lives and applicable conventions, differentiating, for example, between “real property (buildings, etc.) and personal property (equipment, etc.).” Adhering to these stipulated tax lives and methods ensures that businesses and individuals accurately calculate their depreciation deductions, aligning with regulatory requirements. For taxpayers, understanding these rules is not just about compliance; it’s about maximizing legitimate deductions and avoiding potential financial pitfalls.

For those who find these regulations daunting, the IRS offers an array of resources designed to help. For simple federal returns in participating states, “Direct File” provides a free, secure online filing option directly with the IRS. For broader eligibility, the “Free File” program allows taxpayers to prepare and file federal returns using software or fillable forms at no cost. These online tools empower individuals to take control of their tax preparation with confidence.

Moreover, invaluable in-person and phone support programs are available for specific needs. The “Volunteer Income Tax Assistance (VITA) program offers free tax help to people with low-to-moderate incomes, persons with disabilities, and limited-English-speaking taxpayers,” while the “Tax Counseling for the Elderly (TCE) program” specializes in “pensions and retirement-related issues unique to seniors.” Members of the U.S. Armed Forces and qualified veterans can utilize “MilTax,” a free service through Military OneSource. These initiatives underscore a commitment to ensuring all taxpayers have access to the assistance they need.

Read more about: Precision Spending: 12 Budgeting Underdogs That Dominate Financial Debt

Ultimately, mastering depreciation, both in its accounting and tax dimensions, is a powerful tool for financial empowerment. By understanding how assets lose value, how that loss is allocated, and how tax authorities govern its recovery, you are better equipped to make informed decisions about your investments, manage your cash flow, and navigate your tax obligations. Whether you leverage online tools like IRS.gov, seek assistance from community programs, or consult a qualified tax professional, staying informed and proactive is key to securing your financial well-being and making astute choices in an ever-evolving economic landscape.