When you embark on the exciting journey of purchasing a new or even a used car, the primary focus is often on negotiating the vehicle’s price. However, many consumers overlook a critical stage where significant additional costs can quietly accumulate: the dealership’s financing office. This is where a plethora of add-ons and accessories are presented, often with aggressive sales pitches designed to inflate your final bill.

Understanding which of these dealer-offered products and services truly add value versus those that are simply high-markup temptations is paramount to making a financially sound decision. Before you even sit down to sign the paperwork, it’s crucial to equip yourself with knowledge about these potential pitfalls. Many of these add-ons come with questionable value, massive markups, or are readily available from external sources at a fraction of the dealership’s price.

This comprehensive guide aims to shed light on some of the most common and often unnecessary add-ons that car dealerships will try to sell you. We’ll delve into the specifics of each offering, providing objective insights and practical, actionable advice to help you navigate these discussions confidently. Our goal is to empower you, the consumer, to make informed choices, avoid common pitfalls, and ultimately save thousands of dollars on your next vehicle purchase.

1. **Extended Warranties**Extended warranties, often referred to as vehicle protection plans or vehicle service contracts, promise to cover repair costs after the manufacturer’s original warranty expires. While the concept of protecting against catastrophic vehicle failures after the initial warranty period might seem appealing, the reality of purchasing these directly from a car dealer at the time of sale often leads to significant overpayment. Consumers frequently find themselves paying thousands of dollars more than necessary for these contracts.

Manufacturer-backed extended warranties may offer some peace of mind and potentially save money in the event of a major breakdown. However, the market is also flooded with third-party extended warranties and service contracts, which are notorious for their substantial markups and an abundance of fine print. It is virtually impossible to thoroughly research these complex contracts while under pressure in a dealership’s finance office, making on-the-spot decisions a huge mistake that can cost you dearly.

Before considering any extended warranty, insist on examining the actual contract document, not just a glossy brochure that omits crucial details and exceptions. Furthermore, a diligent consumer should investigate the warranty company’s reputation by contacting the Better Business Bureau or other consumer advocacy agencies. Understanding their track record of complaints and how long they’ve been in business can provide invaluable insight into their reliability and trustworthiness. Remember, you are not obligated to purchase an extended warranty at the same time you buy the car, nor are you confined to the dealership’s offerings unless it is the manufacturer’s own program. Explore options from your lender, insurance agent, and reputable online sources to find competitive pricing and suitable coverage. A key consideration is also where service can be obtained; if tied solely to the selling dealership, its value diminishes if you move or the dealer closes. Deductibles and claim approval processes also warrant close scrutiny.

Read more about: The Affordable New Truck That Is Outselling the Ford F-150: Market Dynamics and Unprecedented Value

2. **Rear-Seat Entertainment Systems**For families with children, rear-seat entertainment systems, featuring screens for passengers in the second row, can appear as an attractive solution for keeping kids engaged during long journeys. These systems can be integrated at the factory level as original equipment or installed as aftermarket accessories by the dealership. While the convenience is undeniable, the cost associated with dealership installation, especially for aftermarket systems, often represents poor value for money.

When considering such a feature, a more prudent approach is to seek out vehicles where these systems are offered as a factory-installed option. Factory systems are typically designed to integrate seamlessly with the vehicle’s electrical architecture and interior aesthetics, often at a more reasonable overall cost compared to a dealer-installed aftermarket solution. This also ensures that the system is covered under the vehicle’s primary warranty, simplifying potential service issues.

Alternatively, a far more flexible and often significantly cheaper solution lies in readily available portable electronic devices. Providing children with personal iPads or tablets, coupled with headphones, offers an adaptable entertainment option that isn’t confined to a single vehicle. These devices can be utilized across different cars, during other modes of travel, or even at home, providing greater utility and a substantial cost saving over a fixed, dealer-installed system that may quickly become outdated.

Read more about: Beyond the Buzz: Unpacking the Hidden Nausea of Next-Gen EVs and How Tech is Tackling Car Sickness

3. **Paint and Fabric Protection**Dealerships frequently offer expensive paint sealants and fabric protection packages, often costing hundreds or even thousands of dollars. The sales pitch suggests these treatments are essential for safeguarding your vehicle’s appearance. However, many modern vehicles come from the factory with high-quality paint finishes and interior fabric protection already applied, rendering these additional, pricey dealer add-ons largely redundant and a questionable investment.

One of the primary selling points for these protection plans is an accompanying warranty against damage to the paint or upholstery. Consumers should critically assess whether the exorbitant price of the product justifies the potential repair costs it purports to cover. It’s often the case that the same amount of money, if saved, could cover numerous minor dents or stains without the restrictive clauses and exclusions commonly found in these protection plans, which often limit their actual utility.

For those desiring extra protection not provided by the factory, much more affordable and effective options exist outside the dealership. High-quality car waxes applied frequently can provide excellent paint protection at a fraction of the cost. Similarly, fabric protection can be enhanced by consumer-grade spray-on products, such as Scotchguard, which can be applied independently. It is always advisable to test any such product on an inconspicuous area first to ensure compatibility and desired results.

Read more about: Reality TV’s Reckoning: The Legal and Financial Disasters That Threaten Dynasties

4. **Key Protection**In an effort to introduce new expensive add-ons, dealerships are increasingly highlighting the high replacement cost of modern car keys and key fobs, which are significantly more complex and costly than their predecessors. Consequently, they offer “key protection” plans, often priced at hundreds of dollars, designed to insure against loss or damage. While a new key can indeed cost upwards of $500 to replace and reprogram, paying a couple of hundred dollars to insure it often represents a poor financial decision.

Many mechanical or electrical failures of a car key are likely to be covered under the vehicle’s bumper-to-bumper warranty, negating the need for a separate protection plan. Furthermore, standard automobile insurance policies typically do not cover the loss or damage of car keys. However, it is always recommended to check with your insurance provider, as many companies offer the option to add this coverage at a relatively affordable price as an endorsement to your existing policy, proving a more cost-effective solution than the dealership’s offering.

For those concerned about losing their keys, there are also inexpensive tracking devices that can be linked to smartphone applications, offering a practical solution for locating misplaced items. Additionally, some dealership key protection packages bundle in towing and locksmith services. These same valuable services are often available for less money, and with added benefits like comprehensive roadside assistance, through established automobile clubs such as AAA, providing a superior value proposition compared to the dealer’s limited offering.

Read more about: Beyond the Red Carpet: Inside Ryan Gosling’s Guarded World and the Unwavering Commitment to His Family’s Privacy

5. **Anti-Theft Window Etching**The sales pitch for anti-theft window etching is often presented as a deterrent to car thieves and an aid in vehicle recovery. By etching the Vehicle Identification Number (VIN) onto the car’s glass, dealers claim it reduces the car’s appeal to thieves and facilitates its return if stolen. However, paying a hundred dollars or more for this service at the dealership is largely a waste of money, as the purported benefits are questionable at best.

The reality is that a car thief is unlikely to notice window etching before stealing a vehicle, and if they do, it’s improbable to act as a significant deterrent. Moreover, the VIN is already prominently stamped in multiple locations throughout the vehicle, diminishing the incremental value of adding it to the glass for recovery purposes. This makes the effectiveness of window etching as a theft deterrent or recovery aid largely negligible in practical terms.

Alarmingly, dealerships sometimes pre-print window etching and its associated cost on sales forms, making it appear as a mandatory component of the purchase contract. Consumers should be aware that this is generally not a required item. If you do not desire it, insist that the cost be removed or substantially discounted. Often, these packages also include “theft protection coverage,” which, much like extended warranties, tends to be laden with exclusions that severely limit its practical value and primarily serves to boost the dealer’s markup. For those genuinely interested in VIN etching, DIY kits are readily available online for a minimal cost, allowing for significant savings.

Read more about: Why Your Dream Truck Is Costing You Thousands More: An In-Depth Guide to Unmasking Hidden Dealership Fees and Markups

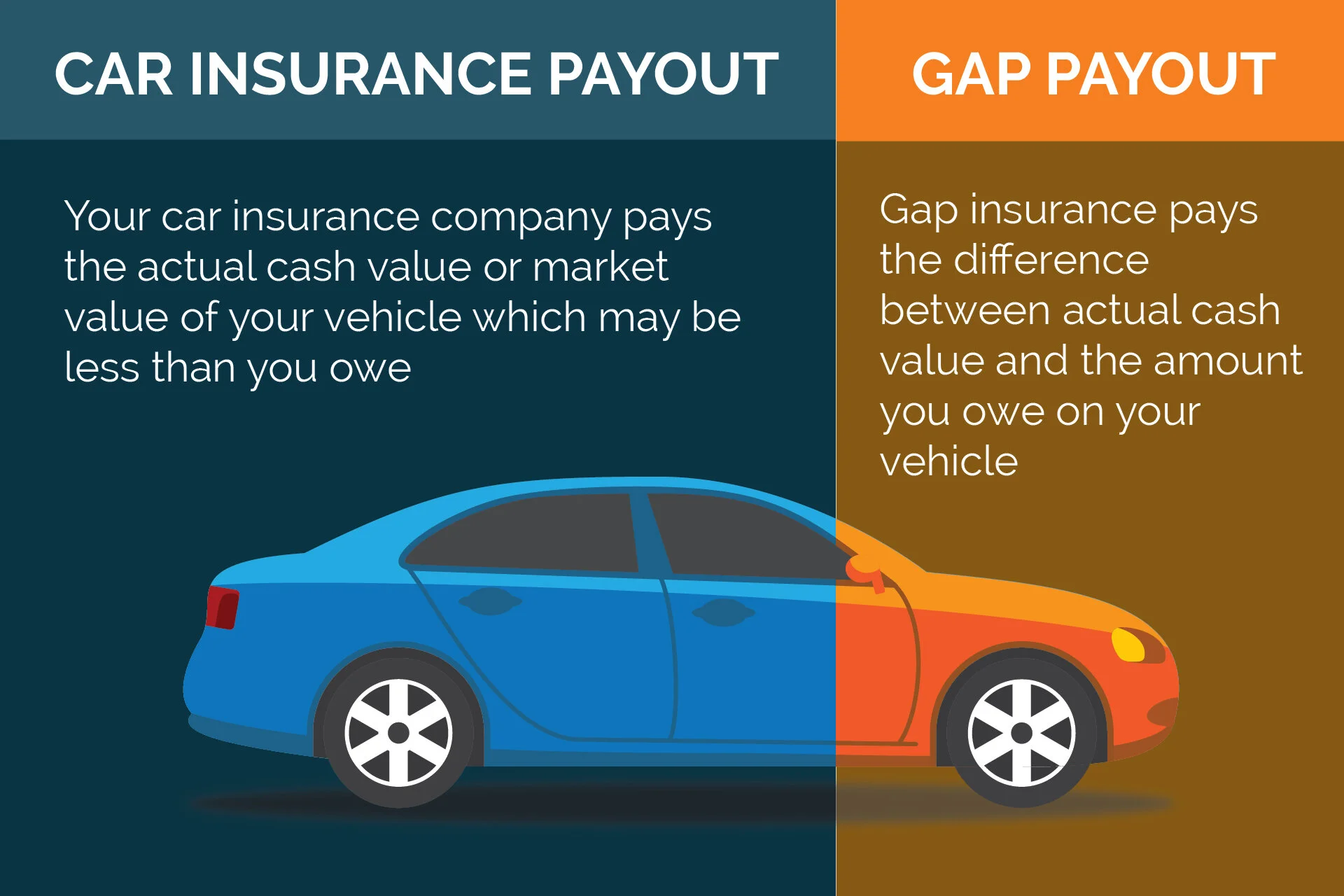

6. **Gap Coverage**Guaranteed Asset Protection, or Gap coverage, is designed to cover the difference between what you owe on your car loan and the vehicle’s actual cash value if it’s declared a total loss or stolen. This is a crucial consideration, particularly for leased vehicles where it’s often a mandatory requirement, and can be a good idea for some buyers, especially if depreciation outpaces loan repayment. However, acquiring it directly from a car dealer without researching alternatives can be a costly error.

Car dealerships often present gap insurance as an essential purchase, and indeed, selling it is a significant profit center for them. Despite the pressure, consumers are not compelled to buy gap coverage from the dealership, even if their lease agreement stipulates it. It is highly advisable to shop around for this coverage. Your own auto insurance company is an excellent place to start, as they frequently offer gap coverage as an affordable add-on to your existing policy, providing precisely the protection you need. Your lender may also offer competitive rates.

When comparing options, price shouldn’t be the sole determinant. It’s vital to meticulously examine what the policy covers, any limitations on that coverage, and the reputation of the company providing the insurance. A critical point to remember is that if you’ve rolled the outstanding balance of a previous car loan into your new vehicle’s financing, gap coverage might not encompass the entirety of your new, inflated loan balance. Once you have a clear understanding of market prices and superior coverage plans, you can then give the dealership an opportunity to match or beat those offers, putting you in a stronger negotiating position.

Read more about: Smart Savings on Wheels: Unveiling the 10 Best Value Used Cars for Frugal Shoppers, Backed by Dealer Insights and Long-Term Records

7. **Nitrogen-Filled Tires**Dealerships may present nitrogen-filled tires as a premium upgrade, citing benefits such as more stable tire pressures due to nitrogen’s lower temperature sensitivity, and a slightly slower rate of pressure loss compared to regular air. These characteristics, in theory, could lead to marginally longer tire life and more consistent tire performance. However, the practical advantages for a typical passenger vehicle often do not justify the hundreds of dollars that dealerships charge for this service.

For race cars, precise and stable tire pressures are indeed critical. But for the average consumer, a fluctuation of a couple of pounds per square inch (PSI) in tire pressure will not have a significant or discernible impact on fuel mileage, drivability, tire wear, or overall safety. The notion that nitrogen eliminates the need for regular tire pressure checks is also a misconception and a potentially dangerous one. Checking tire pressures routinely is not just about maintaining optimal inflation; it’s also a vital opportunity to inspect tires for signs of damage or abnormal wear, which can indicate underlying issues.

If, after considering the marginal benefits, you still prefer nitrogen in your tires, it is far more economical to obtain this service outside the dealership. Many independent tire shops offer nitrogen inflation for just a few dollars per tire, a stark contrast to the dealership’s inflated prices. This common practice underscores the significant markup dealerships apply to a service that offers minimal tangible benefit for most drivers, making it an unnecessary expenditure for the vast majority of consumers.

Read more about: Unmasking the Trust Deficit: Why Car Dealerships Are Struggling to Connect with Today’s Buyers and How They Can Rebuild Confidence

8. **Credit Insurance Products**Dealerships often present credit insurance products with an enticing sales pitch: the plan will pay off your loan in the event of your death or disability, thereby protecting you or your survivors from accumulating debt. While the concept of financial security might seem reassuring, it is essential to recognize that these products primarily serve as a significant profit center for the lender, with the borrower often paying a substantial premium for the coverage. This kind of insurance essentially indemnifies the bank or lending institution, not the individual, directly offsetting their risk with your expense.

These products typically come in two premium structures. One involves a large, upfront payment that covers the loan’s entire duration, which, if financed, means you’ll be paying interest on that insurance cost for years. The alternative is a fee included in your monthly payments that decreases with the loan balance. Before committing to either, thorough research is advisable. Consumers can frequently find more affordable term life and disability policies independently, which offer broader protection and greater flexibility.

An independently secured policy allows you or your family to decide how the proceeds are used—whether to pay off debts, cover other obligations, or be deposited into your bank account or estate. This provides a level of control and financial benefit that a dealership-sold credit insurance product, tied specifically to the car loan, simply cannot match. It shifts the power back to the consumer, offering a more comprehensive and often less expensive safety net.

A related offering sometimes encountered is coverage designed to handle your debt if you become unemployed. Prior to considering such an add-on from a car dealer, it is prudent to consult your current loan provider and car insurance company. They may offer equivalent coverage at a lower cost, or you might find that your existing financial safeguards already provide adequate protection. Importantly, in most states, car dealerships are legally prohibited from mandating these policies as a condition of sale; if a dealer insists, it should be viewed as a significant red flag, prompting you to reconsider the transaction entirely.

Read more about: Beyond the Sticker Price: Unveiling How Car Dealers Secretly Add Thousands to Every Sale Through Financing and Hidden Charges

9. **Factory Roof Rack Accessories**Many automakers provide a proprietary range of roof rack accessories specifically designed to fit their factory-installed racks. While these might appear convenient for those looking to maximize their vehicle’s cargo capacity for outdoor adventures or family trips, opting for these items directly from the dealership can lead to substantial long-term costs. The limited selection and often inflated prices for these brand-specific accessories warrant a careful comparison with aftermarket alternatives before purchase.

A more economical and versatile strategy involves bypassing these dealership-exclusive offerings and instead acquiring accessories from reputable aftermarket rack companies such as Thule or Yakima. These industry leaders provide a vast array of universal accessories, often accompanied by adapter kits that enable them to integrate seamlessly with various factory crossbars. The financial savings realized by choosing these external suppliers are often significant, offering equivalent quality and functionality at a much more competitive price point.

Beyond the immediate cost savings, the advantages of choosing third-party rack accessories extend to their adaptability and broader selection. Unlike proprietary dealership items, generic rack accessories can be easily transferred from one vehicle to another, eliminating the need to repurchase new equipment when you upgrade your car. Furthermore, the sheer multitude of available accessories from specialized rack manufacturers far surpasses the typically limited selection found at a dealership, allowing consumers to find precisely the right solution for their specific needs, whether it’s for bikes, kayaks, skis, or cargo.

While some automakers are beginning to incorporate parts from well-known aftermarket brands like Thule and Yakima into their factory rack systems, the initial prices at the dealership may still be higher than what you would find at sporting goods stores or through online retailers. Though the dealership might offer the convenience of including the purchase price in your car’s financing and potentially covering these parts under the car’s warranty, the overall value proposition often remains stronger when sourcing these components independently, especially when considering the long-term utility and cost efficiency.

Read more about: The Untapped Car Insurance Loophole That Could Slash Your Premiums by Up to 45 Percent This Year

10. **Windshield, Tire & Wheel, or Dent Protection**Car dealerships frequently offer various protection packages, including plans that specifically cover a vehicle’s glass, tires and wheels, or provide for small dent repairs on the bodywork. These packages are presented as a safeguard against unforeseen damage and repair costs. However, for the majority of car buyers, a more financially prudent approach is to set aside the money that would be spent on these plans and use it to cover any repairs should they actually become necessary.

If you find yourself considering one of these protection plans, it is absolutely crucial to look beyond the appealing imagery and promises found in glossy sales brochures. Insist on examining the actual contract documents that underpin these programs. All too often, you will discover an extensive list of conditions, exclusions, and limitations that dramatically reduce the practical value and scope of the coverage, making them far less beneficial than initially advertised.

Before committing to any such plan, it is also highly recommended to investigate the health and reputation of the companies providing the coverage. This can be done by searching their name online and by contacting the Better Business Bureau or other consumer advocacy groups in their operational area. Understanding their track record of customer satisfaction and complaint resolution can provide invaluable insight into the reliability and effectiveness of their protection services.

Dealerships may also promote specialized windshield protection treatments, claiming they strengthen and safeguard your vehicle’s glass. A fundamental question to pose is this: if such a universally effective and affordable substance truly existed, wouldn’t vehicle manufacturers be integrating it into all their cars as a standard feature? While typical comprehensive auto insurance policies do not cover all types of road damage, most common forms of damage are indeed covered. For those specific types of damage not covered, you will almost certainly be better off financially by bypassing the dealership’s packages and retaining your funds to address any issues independently, should they arise. Be particularly wary of any sales consultant who asserts that these protection packages are mandatory for all vehicles sold; such a claim is highly suspect and often a clear indication that you should explore other dealerships.

Read more about: For Snow Belt Residents: A Deep Dive into the 10 Worst Winter-Ready Vehicles on the Market Today

11. **Tire and Wheel Packages**Stepping onto a car dealership showroom floor often reveals vehicles prominently displayed with upgraded or aftermarket tire and wheel packages. These visually appealing enhancements are typically listed with their additional costs on addendum stickers, positioned right alongside the vehicle’s official manufacturer’s window sticker. While these custom wheels can significantly enhance a car’s aesthetic appeal, their inclusion often comes with a substantial price premium that may not align with every buyer’s preferences or budget.

If you are interested in a particular vehicle but not the expensive, upgraded wheels, it is essential to engage in direct negotiation to have them removed. While salespeople might initially be reluctant, the original, standard tires and wheels are almost certainly stored somewhere in the dealership’s service shop. Be firm in your request, and do not accept the vehicle with the upgraded wheels if you do not want them, unless you can negotiate a price that makes them worthwhile. If the dealership agrees to reinstall the original wheels, ensure that this swap is completed and verified before you sign any final paperwork, preventing potential complications down the line.

Prior to purchasing custom tires and wheels through a dealership, a thorough evaluation of various factors is critical. Research whether any warranties provided by the dealer match or exceed the original coverage for the stock tires, wheels, and the essential tire pressure monitoring system sensors. It is also highly advisable to investigate what a similar package would cost if purchased outside the dealership, from specialized tire stores or reputable online retailers such as Tirerack.com. This comparative shopping can reveal significant cost disparities and offer a broader range of options.

By exploring external sources, you gain the distinct advantage of selecting the precise wheels and tires that best meet your aesthetic preferences, performance requirements, and budget, rather than being limited to the specific combination that happens to be on display in the showroom. This approach empowers you to make a more informed and personalized decision, often resulting in superior value and greater satisfaction with your chosen upgrades.

Read more about: America’s Iconic Sports Car: Decoding the Most Problematic Corvette Models in History to Help You Buy Smart

12. **Window Tinting and Clear Film Protection**In many climates, automotive window tinting is not merely an aesthetic choice but a practical necessity, offering benefits such as reduced interior heat, improved privacy, and enhanced security by making it more difficult for potential thieves to view valuables inside the vehicle. However, opting for window tinting services directly at the dealership can often result in significant overpayment, as their prices tend to be higher than those of independent specialists.

For consumers considering window tinting, the most advisable course of action is to make comprehensive price and product comparisons from multiple independent retailers. This proactive approach allows you to identify competitive pricing and ensure that you are receiving a high-quality product that meets your specific needs. The same diligent research applies to plastic film protection products, commonly known as Clear Bra. These films vary significantly in quality, durability, and performance, and a thorough investigation is essential.

It is highly recommended to search online for reviews and recommendations regarding which products are performing best for vehicle owners in your specific geographical area. Performance can differ based on local environmental conditions, so understanding regional experiences can guide your choice toward a product that offers optimal longevity and protection. This consumer-focused research ensures you invest in a solution that is both effective and durable, providing real value for your money.

A paramount consideration for both window tinting and transparent protection films is the quality of installation. Proper application is vital for the film’s appearance, longevity, and effectiveness. A shop that specializes in these installations, performing them frequently and with trained technicians, is invariably a better choice than a general dealership service department that only occasionally applies such products. Expert installation minimizes the risk of bubbles, peeling, or other imperfections, ensuring a professional finish that truly protects your vehicle.

Read more about: Unmasking Dealer Markups: The Essential Guide to Avoiding Costly Car Add-Ons and Protecting Your Wallet

13. **Car Alarms and Tracking Systems**Before committing to an alarm system or a vehicle tracking system, such as LoJack, through a car dealership, it is always prudent for consumers to thoroughly shop around at dedicated car electronics retailers. These specialized stores often offer a wider selection of security products, potentially at more competitive prices, and may have systems that are better tailored to your specific needs and security concerns, assuming you determine that an aftermarket system is indeed necessary.

It is a common practice for some dealerships to install security systems on every vehicle present on their lot. This is primarily done as a measure to deter theft from their inventory. Subsequently, when a vehicle is purchased, the dealership will attempt to sell the pre-installed system to the buyer. If you do not want this additional security system, it is crucial to insist that it be removed in its entirety, or that its cost be substantially discounted, before you finalize the purchase agreement. If you are special ordering a vehicle, a proactive step is to specifically request that the dealer refrains from installing any such security system upon its arrival.

It is also worth noting that many new cars today come standard with sophisticated alarm systems directly from the factory. Furthermore, a growing number of vehicles are available with integrated telematics systems, such as Chevrolet OnStar, Kia Connect, or Hyundai BlueLink. These advanced systems often include comprehensive vehicle tracking capabilities as part of a monthly subscription fee, providing a built-in security and connectivity solution that may negate the need for an additional aftermarket alarm or tracking device.

Understanding your vehicle’s existing security features and exploring these integrated options can help you avoid unnecessary expenditures on redundant or less effective aftermarket systems. By empowering yourself with knowledge about available alternatives, both factory-installed and through specialized retailers, you can make an informed decision that truly enhances your vehicle’s security without falling victim to high-pressure sales tactics.

Read more about: Unpacking the Unsettling Rise in Car Thefts: A Consumer Reports Guide to Understanding and Protecting Your Vehicle

14. **Delivery Fees**A delivery fee, while not technically an add-on product in the same vein as an extended warranty or paint protection, represents another significant charge that consumers should scrutinize and, in most cases, actively avoid paying at the dealership. This fee is a relatively recent tactic employed to potentially trick buyers into paying twice for a service that is already comprehensively covered within the vehicle’s advertised price.

Often, this additional delivery fee will only surface when you are in the final stages of signing the paperwork, a point where many buyers are fatigued and eager to complete the transaction. The amount listed for this separate delivery fee will typically be identical or very similar to the “destination charge” that is already clearly shown on the vehicle’s manufacturer’s price sticker. Many unsuspecting shoppers, either due to oversight or confusion, end up paying both fees, effectively doubling the cost of vehicle transport.

It is imperative to understand that if anyone at the dealership attempts to explain a separate “delivery fee” as the cost of having the car shipped from the manufacturer to the dealer’s lot, they are providing dishonest information. The legitimate and comprehensive cost of shipping the car to the dealership is already included and specified within the “destination fee” on the manufacturer’s official price sticker. This charge covers the logistics of getting the vehicle from the factory to the sales floor and is non-negotiable as it’s set by the manufacturer.

Therefore, if you encounter a separate, additional “delivery fee” listed on your purchase agreement, you must unequivocally ask to have it removed. Should the dealership refuse to eliminate this redundant charge, it should be considered a clear signal to re-evaluate the deal entirely. At this juncture, walking away from the transaction is a powerful consumer action that demonstrates your awareness and refusal to be subjected to deceptive pricing practices. Your informed stand can save you hundreds of dollars and ensure a more transparent purchasing experience.

**The Path to a Smarter Car Purchase: Avoiding Dealership Overcharges**

Navigating the complexities of a car purchase extends far beyond just negotiating the vehicle’s sticker price. As we’ve thoroughly explored, the financing office is a critical arena where unsuspecting buyers can incur thousands of dollars in unnecessary expenses through a myriad of dealer add-ons and inflated service charges. From credit insurance products that primarily benefit the lender to redundant delivery fees that essentially double-charge for transport, the landscape is fraught with opportunities for dealerships to boost their profits at the consumer’s expense.

The core message is one of empowerment through information. Equipping yourself with detailed knowledge about these common dealership tactics is your strongest defense. Always insist on seeing actual contract documents, rather than relying on glossy brochures, and thoroughly research any product or service the dealership attempts to sell you. Compare prices and offerings from independent retailers, your insurance provider, or specialized online sources. You are never obligated to make an immediate decision, and pressure tactics are precisely that—tactics designed to bypass your rational judgment.

Read more about: Navigating the Crossroads: Key Legal and Policy Shifts Redefining the Trucking Industry in 2025

Remember, the goal is to drive away in your new vehicle with confidence, knowing you’ve made financially sound decisions, not just on the car itself, but on every single component of the purchase. By being prepared, questioning every additional charge, and being willing to walk away if a deal feels exploitative, you can safeguard your finances and ensure that your exciting new car purchase remains a celebration, free from costly regrets. Your diligent research and firm negotiation are the keys to avoiding these expensive dealer add-ons and truly optimizing your investment.