The allure of early retirement often paints a picture of serene mornings, endless travel, and the freedom to pursue passions unfettered by the demands of a daily grind. Imagine exchanging that packed train commute for the simple pleasure of alphabetizing your spice shelf, or perhaps embarking on a long-awaited adventure. This dream, while captivating, remains just that for many; only 13 percent of today’s workers plan to retire before age 60, according to an Employee Benefit Research Institute (EBRI) survey. For those who do take the plunge, the reality can diverge significantly from the fantasy, underscoring the critical need for meticulous planning.

Before you decide to step away from the workforce ahead of the traditional retirement age, it’s essential to rigorously evaluate both the liberating advantages and the serious financial and social challenges that accompany such a momentous decision. This isn’t just about accumulating enough savings; it’s about understanding the intricate web of healthcare costs, investment growth, Social Security implications, and even the psychological adjustments required to truly thrive in an extended retirement. Our goal is to provide you with the clear, actionable insights needed to make an informed choice that aligns with your financial well-being and life aspirations.

In this comprehensive guide, we’ll explore the multifaceted aspects of retiring early versus continuing your career for a longer period. We will break down the key considerations, from reclaiming your time and improving your personal well-being to navigating complex financial landscapes like healthcare expenses and the nuances of Social Security benefits. By examining these crucial factors, you’ll be better equipped to evaluate the advantages and disadvantages, and ultimately, lay out a strategy that is best suited for your unique circumstances and financial future.

1. **Freedom from Office and Work Schedule Constraints**Stepping away from the daily demands of a full-time job offers an unparalleled sense of liberation, allowing you to reclaim control over your most precious asset: your time. No longer bound by early mornings, rigid office hours, or the dreaded rush-hour commute, you gain the autonomy to shape each day according to your own desires. This fundamental shift means saying goodbye to reporting to a boss and instead using your time precisely as you choose, whether for personal enrichment or newfound adventures.

Ray Prospero, a partner advisor at AdvicePeriod in the Los Angeles area, highlights this transformative aspect, noting, “Many early retirees embrace the nomadic lifestyle and use their newfound freedom to travel, explore and see the world.” This freedom extends beyond travel, encompassing the ability to simply decide what you want to do with your day, without the need for permission or the constraints of a corporate calendar. It’s an opportunity to truly live life on your own terms.

The flexibility inherent in early retirement also opens doors to a more adaptable lifestyle. You can set your own pace, choosing when to be busy and when to relax. This freedom from external schedules is often one of the most compelling motivations for individuals considering an earlier exit from the workforce, offering a tangible improvement in daily quality of life and personal autonomy.

Read more about: Beyond the Box Office: Why the ‘No-Budget’ Film is Required Viewing for Every Aspiring Filmmaker

2. **More Time to Pursue Passions and Hobbies**With the demanding schedule of a career behind you, early retirement presents an invaluable opportunity to dedicate yourself to long-neglected passions, cultivate new hobbies, and engage deeply with your community. This newfound availability allows you to explore activities that bring profound personal satisfaction and fulfillment, enriching your life in ways that might have been impossible during your working years. Whether it’s picking up a paintbrush, learning a musical instrument, or diving into a complex gardening project, the time is finally yours.

Many retirees find themselves more engaged and active than ever before. Jonathan DeYoe, senior vice president and partner at EP Wealth Advisors and author of “Mindful Money,” shares this observation, stating, “Many retirees I have worked with say they are busier in retirement – with personal and philanthropic work – than they were before they retired.” This highlights the potential for early retirement to be a period of intense engagement and contribution, rather than mere leisure.

The freedom to pursue these interests also extends to volunteering and civic involvement. If you’ve been waiting for the chance to contribute to your community, early retirement provides the perfect opportunity to do so, offering a powerful sense of purpose and connection. This dedicated time for personal and philanthropic work can become a central pillar of your post-career identity, providing structure and meaning that replaces the professional roles you’ve left behind.

Read more about: Unmasking the Truth: 10 Costly Retirement Lies You Need to Stop Believing for a Secure Future

3. **Improved Physical and Emotional Well-being**One of the most significant, though often underestimated, benefits of early retirement is the profound improvement it can bring to your physical and emotional well-being. The stresses, long hours, and sedentary nature of many jobs can take a toll on health, making it challenging to prioritize self-care. Early retirement fundamentally shifts this dynamic, allowing for a concentrated focus on a healthier lifestyle.

As Danielle Miura, a certified financial planner and founder of Spark Financials, points out, “Sleeping more, stressing less and getting out in fresh air more can be advantageous to your health.” With more time at your disposal, you can consistently engage in physical activities like hiking, gardening, or yoga, directly boosting your fitness levels. This deliberate attention to exercise and healthy eating, often difficult during working years, becomes a cornerstone of your daily routine, leading to a stronger and healthier body.

Beyond the physical, emotional well-being often sees a remarkable uptick. The absence of work-related stress, demanding deadlines, and workplace politics can foster a sense of peace and tranquility. This reduced stress, combined with more opportunities for social interaction with family and friends, helps to combat feelings of isolation and contributes to a more relaxed and contented state of mind. Ultimately, early retirement can open doors to a happier life, one that is richer in experience and joy.

Read more about: Beyond the Headlines: Angelina Jolie’s Unyielding Journey Through Hollywood, Humanitarianism, and Personal Trials

4. **Opportunities for Travel and Leisure**With improved health and emotional balance firmly in place, early retirement naturally unlocks a world of opportunities for travel and leisure, transforming long-held dreams into tangible realities. The absence of a full-time job schedule eliminates the need to meticulously plan trips around vacation days, freeing you to explore the world, embark on extended adventures, or simply enjoy local attractions at your own pace. Many envision this as a core component of their retirement.

This flexibility is a major perk, allowing you to take that long-awaited vacation without constraints. You can revisit beloved destinations, discover new places you missed while working, or simply enjoy spontaneous getaways. Traveling at your own pace means no more rushing through itineraries; you can linger in interesting locales, truly immersing yourself in new cultures and cuisines, enriching your life experiences significantly.

Furthermore, the ability to travel without strict timelines makes visiting family and friends much easier and more frequent. Without work commitments holding you back, you can dedicate quality time to strengthen these important relationships. This blend of global exploration and personal connection makes leisure in early retirement a deeply rewarding experience, contributing immensely to a fulfilling post-career life.

Read more about: Unmasking the Truth: 10 Costly Retirement Lies You Need to Stop Believing for a Secure Future

5. **The Chance to Choose Additional Work or Start a New Business**Early retirement doesn’t necessarily mean an end to all work; rather, it often signifies a transition to a more flexible, personally fulfilling form of work. Many individuals find that the freedom of early retirement inspires them to pursue a new career or start a business based on their true passions, converting what they love into a rewarding endeavor. This can be a powerful way to maintain engagement and purpose while still enjoying increased autonomy.

As Brendan Sheehan, managing director of Waymark Wealth Management, aptly puts it, “If you want to work, you can still work, but on your own schedule.” This ability to dictate your terms, whether it’s a part-time role, consulting, or an entrepreneurial venture, allows you to leverage your unique skills and experience without the stress of a full-time commitment. In some cases, if a potential employer highly values your expertise, you may even find yourself earning more than you did in your previous career.

This period of life offers a prime opportunity for personal and professional growth in unexpected ways. You gain the time to learn new skills, engage with different communities, and build something entirely new, free from the pressures and constraints of a traditional job. The freedom that comes with retiring early empowers you to make these choices deliberately, ensuring that any work you undertake truly aligns with your personal values and lifestyle preferences.

Read more about: Decoding the ‘No-Haggle’ Deception: 12 Insider Secrets Car Dealers Hope You Never Learn

6. **High Healthcare Costs Before Medicare Eligibility**While the allure of early retirement is strong, a significant practical hurdle for many is the substantial cost of healthcare before becoming eligible for Medicare. This federal program, which provides health coverage for over 65 million older Americans, doesn’t typically begin until age 65. Consequently, if you retire earlier, you’ll need to secure an alternative, and as many financial experts caution, it certainly won’t come cheap.

Brian Schmehil, director of wealth management for the Mather Group in Chicago, states candidly, “Private health insurance before Medicare kicks in costs an arm and a leg.” Even with current laws stipulating that insurance costs can’t exceed 8.5 percent of household income, the figures remain substantial. For instance, a single person earning $54,360 might face monthly costs of $385 for a mid-level silver plan, translating to $4,620 annually. These substantial premiums can quickly become a major drain on retirement savings.

This potential health insurance crunch is a critical consideration. Danielle Miura notes that “Depending on your age and income, marketplace insurance policies can be very expensive.” If you are a federal employee, the circumstances might be different, as you might get to keep FEHB, but for most, bridging this gap with private insurance can be a substantial financial burden. These high costs highlight the necessity of robust financial planning specifically for healthcare expenses in the years leading up to Medicare eligibility.

Read more about: Beyond the Average: A Comprehensive Guide to Understanding and Planning for the $172,500 Healthcare Costs Facing Retirees

7. **Early Penalties and Taxes on Retirement Accounts**One of the most immediate and impactful financial drawbacks of retiring early is the potential for costly penalties and taxes associated with tapping into your nest egg prematurely. If you decide to retire and begin withdrawing funds from most tax-deferred accounts, such as traditional IRAs and 401(k) plans, before the age of 59 ½, you will generally incur a 10 percent early withdrawal penalty. This can significantly erode your carefully saved funds, making each dollar withdrawn less efficient.

Matt Stephens, founder of AdvicePoint in Wilmington, North Carolina, warns that while “There are some options for getting IRA money before 59 1/2, but it’s tricky and can cause major penalties if done incorrectly.” Navigating these rules requires expert guidance to avoid potentially disastrous financial missteps that could undermine your retirement security. The complexity involved means careful consideration is paramount before making any early withdrawals.

Furthermore, unless you are withdrawing from a Roth IRA, which is funded with after-tax contributions, you will also owe income taxes on the amount you withdraw from traditional accounts. These accounts were funded with pretax contributions, meaning every dollar withdrawn is treated as taxable income. To illustrate the impact, if you withdraw $20,000 from a traditional IRA before age 59 ½ and are in the 15 percent federal tax bracket, you would face a total of $5,000 in taxes and penalties, leaving you with only $15,000 from your initial withdrawal. This dual impact of penalties and taxes underscores the importance of carefully timing your access to retirement funds.

The presence of these penalties and taxes means that early retirement requires not just sufficient savings, but also a strategic plan for how and when those savings will be accessed. Without meticulous planning, a significant portion of your nest egg could be lost to avoidable fees and taxes, reducing the longevity and security of your retirement income. Understanding these rules is a cornerstone of responsible early retirement planning.

Continuing our in-depth look at the complex decision of early retirement, we now shift our focus to the longer-term financial ramifications and psychological adjustments that often prove just as critical as the initial financial hurdles. While the immediate costs of healthcare and early withdrawal penalties are significant, the sustained impact on your nest egg, Social Security benefits, and even your sense of self-worth can shape the success and fulfillment of your golden years. Understanding these profound long-term implications is paramount for anyone contemplating stepping away from the workforce sooner rather than later.

Read more about: Maximize Your Future: The Salary & Strategies to Claim Social Security’s Top $6,450 Monthly Benefit

8. **Sacrificing the Power of Compounding Interest**One of the most powerful allies in your retirement savings journey is time, specifically the phenomenon of compounding interest. Retiring early, by its very definition, shortens the period during which your investments can grow exponentially, dramatically impacting your eventual wealth. This isn’t just about stopping contributions; it’s about losing the momentum of “interest earned on the interest that has compounded.”

Consider the illustrative example: saving $250 a month — $3,000 a year — from age 25 to age 55 could yield approximately $237,000, assuming no withdrawals and an average 6 percent annual return. This seems like a respectable return on $90,000 in contributions. However, the true magic unfolds with an extended timeline.

If you were to work just 10 more years, retiring at 65 instead of 55, that figure nearly doubles to about $464,000. The additional $30,000 in contributions over that decade certainly helps, but the vast majority of that nearly quarter-million-dollar difference comes from the extra 10 years of compounding. Your money has more time to grow, building upon itself, demonstrating that “time is your friend when you are saving for retirement, but not when you are spending.”

Early retirement means cutting this growth period short, potentially leaving hundreds of thousands of dollars on the table over the course of what could be a very long retirement. This substantial opportunity cost highlights why diligently projecting your financial needs over an extended retirement horizon is absolutely critical.

Read more about: A Financial Advisor’s Blueprint: 15 Essential Investment Strategies for a Secure Retirement in 2025

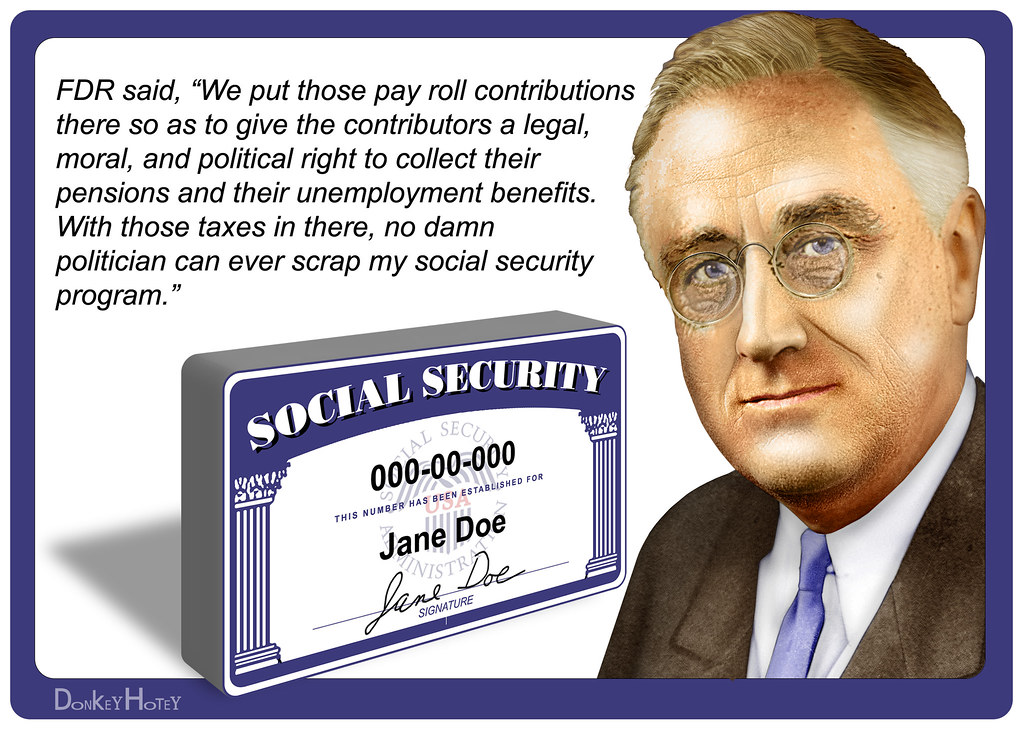

9. **Permanently Reduced Social Security Benefits**Deciding when to claim Social Security benefits is one of the most pivotal financial choices for retirees, and opting to do so early carries a permanent reduction in your monthly payout. The earliest you can start receiving Social Security retirement benefits is age 62, but doing so means accepting a significantly smaller check for the rest of your life. This reduction is not temporary; it is a fixed percentage off your “full retirement age” (FRA) benefit.

For individuals who claim benefits at age 62, the reduction can be as much as 30% of their full retirement benefit. This means you will receive just 70% of the amount you’re entitled to receive based on your lifetime earnings, every single month. While this might provide immediate cash flow, it comes at a substantial long-term cost, especially given that Social Security benefits typically only amount to “about 40% of your average earnings” to begin with.

This reduction is a critical factor because Social Security is designed to provide a foundational income floor throughout retirement. A permanently reduced benefit means a lower guaranteed income stream that must last for potentially decades. This makes it harder to cover escalating living expenses and unforeseen costs, putting greater pressure on your personal savings to bridge the income gap.

It’s worth noting that if you claimed your benefit early and have a change of heart, there is a “narrow window to stop and restart Social Security benefits.” However, for most, the initial decision largely dictates the benefit amount for their lifetime, underscoring the irreversible nature of this financial choice.

Read more about: Maximize Your Future: The Salary & Strategies to Claim Social Security’s Top $6,450 Monthly Benefit

10. **Smaller Cost-of-Living Adjustments (COLA) and Penalties for Working While Claiming Social Security Early**

Beyond the initial reduction, claiming Social Security benefits early also impacts future cost-of-living adjustments (COLA) and can impose penalties if you continue to work. When you receive a smaller monthly benefit initially, any percentage increase from a COLA will naturally translate into a smaller dollar amount increase compared to someone who waited for their full benefit. This seemingly minor difference compounds over time, eroding your purchasing power further.

For instance, if you are a federal employee retiring early, specifically before age 62, you “won’t receive COLA adjustments on your annuity until you turn 62” (unless you are under Special Provisions). This means your fixed pension amount will steadily lose value against inflation for several years, creating a significant “gap” between your income and rising expenses. Even after age 62, while your FERS pension might receive COLA, the adjustments “are reduced compared to inflation” (again, not for Special Provision FERS), further highlighting the challenge of maintaining purchasing power.

Moreover, if you decide to take Social Security early but still work, there are earnings limits that can further reduce your benefits. For 2025, if you have not reached your full retirement age, “Social Security deducts $1 from benefits for each $2 earned over $23,400.” If you reach your full retirement age during the year, a different limit applies: “Social Security deducts $1 from benefits for each $3 earned over $62,160 until your full retirement age.”

While you will eventually “get your money back after you reach full retirement age,” this penalty means less disposable income in the interim, contradicting the very purpose of claiming benefits early for financial relief. These rules illustrate the complex interplay between early claiming, continued employment, and the goal of maximizing your retirement income, demanding careful strategic planning.

11. **Financial Strain from Extended Retirement Years and Risk of Depleting Savings**One of the most daunting financial challenges of early retirement is simply making your savings last for an extended period. Retiring earlier means your “nest egg” must support you for many more years, increasing the “risk of running out of retirement savings.” This extended timeline introduces “more variables and opportunities for a financial plan to go sideways,” as Ray Prospero from AdvicePeriod wisely points out.

The math is straightforward: if you stop working at 55 instead of 65, your retirement funds need to stretch for an additional decade before even considering factors like increased longevity. This longer period of withdrawal, coupled with a shorter period of investment growth, creates substantial “financial strain.” Expenses, particularly healthcare costs, tend to “rise too, especially as you get older,” further burdening your budget.

If your primary sources of income, such as a FERS pension, remain flat without adequate COLA adjustments, while deductions like “health insurance increases annually,” your net retirement income will inevitably “decrease over time.” This highlights a critical, often underestimated, risk: inflation can quietly erode your purchasing power, making it harder to cover essentials like “housing, healthcare, and groceries.”

Therefore, simply having “enough money set aside” isn’t enough; you need a robust financial plan that accounts for inflation, rising expenses, and the potential for a very long retirement. The goal isn’t just to retire early, but to ensure your financial security endures throughout every year of your post-career life.

Read more about: Navigating the High-Mileage Minefield: 10 Cars That Become Costly Money Pits After 100,000 Miles – Essential Consumer Advice to Avoid Costly Mistakes

12. **Loss of Structure, Purpose, and Identity**Beyond the financial considerations, early retirement presents significant psychological adjustments, chief among them the potential “loss of structure and purpose.” For many, a career provides not just income but also a daily routine, intellectual engagement, and a fundamental sense of identity. Stepping away from this framework can lead to unexpected feelings of aimlessness or emptiness, even after achieving the dream of early freedom.

Brendan Sheehan, managing director of Waymark Wealth Management, observes that retirees “often experience an identity crisis.” If your career was a large part of who you are, the sudden absence of that role can be disorienting. Days that once had a clear schedule and defined goals may now “blend together and feel empty,” making it “hard to adjust without work schedules.”

This transition requires more than just financial preparation; it demands a proactive plan for how you will spend your newfound time. As the context suggests, to avoid feeling a “loss of purpose,” it’s essential to “create a plan for how you’ll spend your time. Whether it’s volunteering, starting a business, or pursuing a long-neglected hobby, having a clear sense of purpose can make early retirement more fulfilling.” Without a clear “new chapter planned,” finding contentment can be a significant challenge.

The psychological aspect is so crucial that it can dictate the overall happiness of your retirement. Successfully navigating this shift involves intentionally cultivating new sources of meaning, engagement, and contribution, ensuring that your life remains rich and purposeful even without the demands of a traditional job.

Read more about: Busting the 10 Biggest Myths About Vocal Training, Feat. Music’s Top Icons!

13. **Potential Feelings of Isolation and Loneliness**Another profound, often overlooked, psychological challenge of early retirement is the potential for “feelings of isolation and loneliness.” The workplace often serves as a primary source of social interaction and community. When individuals leave their full-time jobs, they can suddenly find themselves cut off from daily interactions with coworkers and a built-in social network.

Danielle Miura, a certified financial planner, notes that “office environments tend to create a natural setting for social engagement.” Without this routine interaction, the “shift can create a gap in social activities,” leading some retirees to feel “alone more often than before.” This social disconnection can weigh heavily on emotional well-being, especially if friends and peers are still actively engaged in their careers and may not “understand and support your lifestyle.”

Furthermore, as Miura points out, “Retiring early may be perceived by others as being lazy or unmotivated,” which can further exacerbate feelings of social disconnect. To counteract this, it becomes vital for early retirees to intentionally cultivate new social connections and schedule activities that involve others. “Finding part-time jobs or volunteering may help bring back some purpose” and provide new avenues for social engagement.

The context wisely advises, “If you don’t schedule activities that involve others, you could soon feel bored, lonely or disengaged with your community.” Proactively building a robust social life and integrating into new communities is just as important as financial planning for a truly fulfilling early retirement.

Read more about: 9 Behind-the-Scenes Truths: Unpacking the Sincere Grief and Emotional Journeys of Automotive Heroes