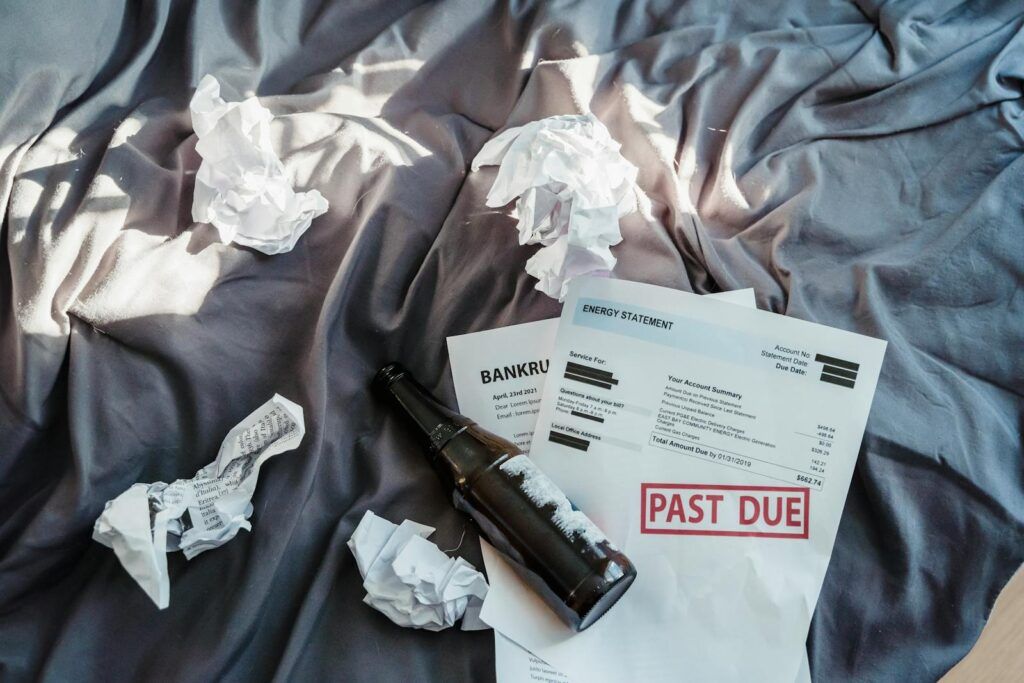

Debt is an intrinsic part of modern financial life, encompassing everything from the smallest credit card balance to the significant commitment of a home mortgage. While often viewed with apprehension, debt itself is a neutral tool that can either build financial strength or create substantial challenges. Understanding its nuances and mastering effective repayment strategies is not just prudent; it’s a pathway to significant savings and peace of mind.

Indeed, for many Americans, navigating the labyrinth of outstanding obligations can feel overwhelming, with interest charges steadily eroding their hard-earned money. The good news is that with the right knowledge and a disciplined approach, individuals can reclaim control over their finances. The goal isn’t merely to pay off what’s owed, but to do so strategically, minimizing the financial burden and ultimately saving a substantial sum – potentially thousands of dollars in interest alone.

This article aims to demystify the world of debt, transforming it from a source of anxiety into an area of actionable opportunity. We will explore various forms of debt, dissect their characteristics, and most importantly, equip you with practical, actionable strategies to manage, reduce, and eventually eliminate your obligations. Our journey begins with building a foundational understanding of debt itself, then moves into targeted approaches for common debt types, and finally underscores the indispensable power of a personalized budget.

1. **Understanding Your Debt Landscape**At its core, debt is simply something owed by one party to another, typically money. However, this simple definition belies a complex financial instrument with both distinct benefits and potential drawbacks. Recognizing these facets is the crucial first step toward effective debt management, allowing individuals to leverage its advantages while mitigating its risks.

On the beneficial side, debt, particularly with a lower interest rate, can be a powerful tool for investing in valuable assets that enhance your long-term financial position. Think of a mortgage that helps you acquire a home, a tangible asset, or student loans that fund a college education, a direct investment in your human capital. Furthermore, consistently borrowing money and repaying it on time is a foundational method for building a strong credit history, which is essential for future financial endeavors.

Conversely, the downsides of debt become apparent when it consumes too large a portion of your monthly income. Financial experts often suggest that if more than about a third of your income is allocated to debt payments, it can become exceedingly difficult to meet all your financial obligations. This precarious situation can also hinder your ability to secure additional credit should the need arise. Moreover, in an environment of rising interest rates, existing variable-rate debt can quickly become more costly, accelerating its growth and making repayment significantly harder.

To navigate this landscape, it’s essential to be familiar with key debt terms. The **Annual Percentage Rate (APR)** represents the yearly cost of borrowing, encompassing both the interest rate and any associated fees. **Collateral** refers to an asset pledged to secure certain loans, which a lender can seize if repayment fails. **Debt consolidation** is the act of combining multiple debts into a single, often more manageable, debt. **Default** signifies a failure to pay, while **delinquency** refers specifically to a late payment. **Interest** is the cost of borrowing, charged by the lender and paid by the borrower, and the **principal** is the original amount borrowed. Finally, the **repayment term** defines the period within which the borrower must repay the debt.

Debt is broadly categorized into two types: secured and unsecured. **Secured debt** is backed by an asset, or collateral, that the borrower pledges. Should the borrower fail to repay as agreed, the creditor has the right to seize this asset. Common examples include auto loans, where the car itself is the collateral, mortgages, where the home serves as collateral, and home equity loans. In these cases, non-payment can lead to repossession or foreclosure, underscoring the serious implications of secured debt.

**Unsecured debt**, on the other hand, lacks this direct asset backing. However, this absence of collateral does not grant immunity from the consequences of non-repayment. For instance, a credit card issuer may attempt to collect the debt through internal departments or sell the delinquent account to a third-party debt collector. These collection efforts can result in persistent contact and, if unsuccessful, may escalate to a lawsuit, potentially leading to wage garnishment. Examples of unsecured debt include credit cards, personal loans, student loans, medical bills, and utility bills. Understanding these distinctions is paramount for effective debt strategy.

Finally, the concept of “good debt” versus “bad debt” is a common one, though debt is not officially classified this way. Some debt is considered more worthwhile because it facilitates the achievement of personal aspirations or has the potential to generate long-term wealth. Student loans, for example, are frequently viewed as good debt due to their role in enabling higher education and career advancement, while mortgages are often considered beneficial because they lead to homeownership, a significant asset. Conversely, high-interest debt or debt incurred through excessive spending, such as revolving credit card balances, is generally considered “bad debt.” Ultimately, whether a debt is perceived as good or bad hinges on its purpose, its terms, and the borrower’s ability to manage it effectively.

Read more about: The Hidden Engineering of Your Future: Unpacking the Power and Precision of a Last Will and Testament

2. **Mastering Credit Card Debt: Snowball vs. Avalanche**Credit card debt is arguably one of the most prevalent and often most expensive forms of unsecured debt in the United States. Its widespread use, coupled with potentially high interest rates, can quickly transform convenience into a significant financial burden. Recent data underscores this challenge, with Americans’ revolving credit card debt estimated to have reached a staggering $645.88 billion as of June 2025. For individuals carrying such debt, the average amount owed was $10,815, a sum that can generate substantial interest charges over time.

The real sting of credit card debt often comes from its Annual Percentage Rates (APRs), which can frequently range into the teens and even high twenties, depending on one’s credit score. When balances are not paid in full each month, these high APRs mean that a significant portion of your monthly payment goes toward interest, rather than reducing the principal. This cycle can be incredibly expensive and can make escaping credit card debt feel like an uphill battle, emphasizing the urgent need for a strategic repayment approach.

Fortunately, there are two widely recognized and effective methods for tackling credit card debt: the debt snowball and debt avalanche methods. The **debt snowball method** prioritizes psychological wins to maintain motivation. With this approach, you focus on paying off your smallest debts first, while making minimum payments on all other debts. Once the smallest debt is eliminated, you roll the money you were paying on it into the next smallest debt, gradually gaining momentum and building confidence as each debt is conquered. This method is particularly appealing to those who need quick successes to stay engaged in their debt reduction journey.

In contrast, the **debt avalanche method** is a purely mathematical approach designed to minimize the total amount of interest paid over the life of your debts. This strategy dictates that you should prioritize paying off debts with the highest interest rates first, regardless of their balance totals. By aggressively attacking the most expensive debts first, you reduce the overall interest accrual, which can lead to significant savings. While it may take longer to see individual debts disappear, the financial benefit in terms of reduced total cost is often greater, making it an ideal choice for those who are highly disciplined and focused on long-term savings.

Beyond these two primary paydown methods, individuals struggling with credit card debt have several other avenues to explore. Consulting a non-profit credit counseling agency for a debt management plan can provide structured support and potentially lower interest rates on existing cards. If you have multiple debts, investigating debt consolidation might offer a single, more manageable monthly payment. For those with good credit, a 0% intro APR balance transfer credit card could provide a temporary reprieve from interest charges, offering valuable time to pay down the balance. In extreme cases, discussing options with a bankruptcy attorney may be a necessary step to explore legal debt relief.

Read more about: Navigating Your Finances: A NerdWallet Guide to Understanding, Managing, and Conquering Debt

3. **Strategic Medical Debt Management**Medical debt represents a unique financial challenge, often stemming from unforeseen circumstances like accidents or serious illnesses, in addition to routine doctor visits. Unlike other forms of debt, medical bills can appear without warning, are often substantial, and typically lack a clear, standardized repayment structure if immediate payment in full is not possible. This makes strategic management crucial to avoid turning a health crisis into a financial disaster.

One of the most straightforward and advisable ways to manage medical bills you cannot afford to pay immediately is to set up a payment plan directly with the provider. Many hospitals and clinics are willing to work with patients to establish an installment schedule, breaking down the large sum into more manageable monthly payments. This approach demonstrates a good faith effort to resolve the debt and can help prevent the bill from going to collections, which could negatively impact your credit.

Another powerful strategy is to negotiate the balance down. Medical bills often contain errors, and providers may be open to accepting a lower amount, especially if you can pay a lump sum or commit to a prompt payment plan. It’s always worth asking for an itemized bill and scrutinizing every charge. If negotiation feels daunting, hiring a medical bill advocate can be incredibly beneficial. These professionals specialize in reviewing bills, identifying discrepancies, and negotiating on your behalf, potentially saving you a significant amount.

However, one piece of advice stands paramount: no matter how strapped for cash you might be, avoid putting medical bills on a credit card. Most medical providers do not charge interest on outstanding balances, at least not for a considerable period. Transferring this debt to a credit card immediately eliminates this advantage, converting an interest-free or low-fee obligation into a high-interest one. This single action can dramatically increase the overall cost of your medical care, making it significantly more expensive to repay.

Furthermore, medical debt benefits from certain preferential treatment by credit bureaus. For instance, medical debt generally has a longer grace period before it appears on your credit report, and paid medical collections are typically removed from credit reports. This advantageous treatment is entirely lost if the debt is converted into regular credit card debt, which lacks these protections. Therefore, exhausting all other options—payment plans, negotiation, or advocacy—before resorting to a credit card is a critical element of strategic medical debt management.

Read more about: From Riches to Ruin: The Shocking Stories of 10 Celebrities Who Lost It All and Couldn’t Recover

4. **Navigating Student Loan Relief Options**For many recent college graduates, student loan debt is a substantial and long-term financial reality. With the average U.S. household carrying a student debt balance of $56,261 as of June 2025, these obligations often represent one of the largest financial commitments for individuals early in their careers. Understanding the various types of student loans and the relief options available is essential for managing this considerable burden over the years.

Student loans typically fall into two broad categories: federal loans, which are issued or guaranteed by the U.S. government, and private loans, which come from banks, credit unions, and other private lenders. Each category comes with its own set of rules, interest rates, and, crucially, repayment and relief options. Federal student loans generally offer more flexible repayment plans and borrower protections, making it vital to distinguish between your loan types when seeking assistance.

If you hold federal student loans and are experiencing difficulty with payments, your first step should be to call your student loan servicer. They are equipped to discuss various relief options, which can include deferment or forbearance, allowing you to temporarily postpone payments. Another valuable option is to sign up for an income-driven repayment (IDR) plan. These plans adjust your monthly payment based on your income and family size, making payments more affordable and often leading to loan forgiveness after a certain number of years of qualifying payments.

Furthermore, certain federal loan programs offer the possibility of forgiveness, cancellation, or discharge if you meet specific eligibility criteria, such as working in public service or teaching in a low-income area. It’s important to actively research and apply for these programs if you believe you qualify, as they can significantly reduce or eliminate your loan burden. Always remember that applying for federal student loan programs and relief options is free; there is no need to pay a company to do what you can do yourself.

For those with private student loans, the options are typically more limited compared to federal loans, especially when it comes to loan forgiveness or income-driven repayment. Your primary course of action should be to contact your loan servicer directly. They may be willing to work with you on a modified payment plan or offer some form of temporary relief, though this is often at their discretion. To identify your private student loan servicer, you can usually refer to a recent billing statement or check your credit report.

A critical warning for all student loan borrowers: be extremely wary of any companies that promise full debt relief help for a fee. Many of these are scams that charge money for services you can get for free from your federal servicer or that make promises they cannot keep. Legitimate assistance for federal student loans is readily available through official government channels and your federal loan servicer, typically without charge. Always verify the legitimacy of any company offering student loan relief before engaging their services or sharing personal information.

Read more about: 14 Actionable Strategies to Conquer Debt Fast in 2025: Your Step-by-Step Guide to Financial Freedom

5. **Optimizing Personal and Car Loans**Personal loans serve a versatile role in personal finance, often utilized for consolidating high-interest credit card debt into a single, more manageable payment, or to provide cash flow for specific needs such as a home remodel. These loans typically feature repayment terms ranging from two to seven years, with interest rates that can vary significantly, from approximately 7% to 36%, depending on the borrower’s creditworthiness and the lender. While personal loans can be a valuable tool, managing them effectively is key to realizing their benefits.

Should you find yourself struggling to keep up with personal loan payments, proactive communication with your lender is paramount. Many lenders are willing to discuss options such as deferring payments for a short period or placing you on a hardship plan, especially if your financial difficulties are temporary and you reach out before missing payments. Exploring these avenues can provide much-needed breathing room and help you avoid default, which can severely damage your credit score. If independent negotiation proves difficult, consulting the free help of a nonprofit credit counselor can provide expert guidance on budgeting and managing your overall financial situation, offering an objective perspective and potential solutions. In situations where debt becomes overwhelming, speaking with a bankruptcy attorney to understand your legal options is a sensible, albeit serious, consideration.

Car loans represent another significant form of debt for many Americans, and they fall under the category of secured debt. This means the vehicle itself serves as collateral for the loan. A critical implication of this structure is that if you fail to make payments as agreed, the lender has the legal right to repossess the car. With car loans becoming increasingly longer in term and more expensive in total cost, the challenge of paying them off has intensified, making strategic management more important than ever.

If you are facing an expensive car loan or are having trouble meeting your payments, several strategies can help. Refinancing the loan at a lower interest rate or with an extended term can reduce your monthly payments, making them more affordable. However, be mindful that extending the term may result in paying more interest over the life of the loan. Another option, though perhaps more drastic, is to downsize to a less expensive car. Selling your current vehicle and purchasing a more affordable one can significantly reduce your debt burden. Alternatively, leasing a less expensive car might offer a temporary solution for lower monthly costs, though this does not build equity.

The most important action to take if you anticipate missing payments is to talk to your lender immediately. Most car financing agreements permit repossession as soon as you are in default, often without prior notice. By proactively communicating your situation, you may be able to negotiate a temporary payment adjustment or find an alternative solution. If you know you cannot keep up with payments, selling the car yourself before repossession is often the better course of action, as it allows you to pay off the debt, avoid the costs associated with repossession, and prevent a significant negative entry on your credit report. Taking control of the situation can mitigate much of the potential financial damage.

Read more about: Home Refinancing 101: Your Essential Guide to Knowing When to Refinance — And When to Hold Off for Bigger Savings

6. **Addressing Mortgage Payment Challenges**Acquiring a mortgage is typically the single largest personal finance decision an individual will make, representing a commitment that spans decades and involves hundreds of thousands of dollars. As of March 2025, the average American household carried a mortgage balance of $234,060, underscoring the immense financial weight this debt carries. Like car loans, a mortgage is a secured loan, meaning your home serves as collateral. The stark reality is that if you fail to meet your payment obligations, the bank can initiate foreclosure proceedings, ultimately leading to the loss of your property.

Given the severity of potential consequences, understanding your recourse when facing mortgage payment difficulties is absolutely vital. The good news is that there are strategies and programs designed to help homeowners navigate these challenging times. One primary option is to consider refinancing your mortgage. This involves taking out a new loan to pay off your existing mortgage, ideally with more favorable terms such as a lower interest rate or a longer repayment period, which can significantly reduce your monthly payments. However, refinancing usually requires good credit and sufficient home equity.

Another critical avenue for relief is to seek a loan modification or a forbearance period. A loan modification involves permanently changing the terms of your mortgage, such as lowering the interest rate, extending the loan term, or even reducing the principal balance, to make payments more affordable. A forbearance agreement, on the other hand, allows you to temporarily reduce or suspend your mortgage payments for a specific period, providing a temporary reprieve during financial hardship. It’s crucial to understand that forbearance typically requires you to repay the missed payments later, either in a lump sum or through an adjusted payment plan.

The most important piece of advice when struggling with mortgage payments is to contact your lender immediately. Do not wait until you are significantly behind, as delaying action increases the risk of foreclosure. Most lenders are willing to work with homeowners who demonstrate good faith and whose financial situation is temporary. They may offer to lower or suspend your payments for a short time or extend your repayment period. Before agreeing to any new plan, always inquire about any extra fees or potential long-term consequences to ensure it truly benefits your financial situation.

Furthermore, be highly cautious of companies that promise to modify your mortgage or take other steps to save your home but demand upfront fees. Many of these are mortgage assistance relief scams. Never pay a company in advance for such promises. Instead, if you cannot work out a plan directly with your lender, seek assistance from a non-profit housing counseling organization. These organizations, often HUD-certified, can provide free, legitimate advice and guidance. You can reach a free, HUD-certified counselor by calling 800-569-4287, or contact your local Department of Housing and Urban Development office for trusted resources.

Read more about: Navigating the Wealth Landscape: Expert Financial Advisers Guiding America’s Top Athletes to Enduring Success

7. **The Power of a Personalized Budget**At the heart of any effective debt repayment strategy and, indeed, sound financial management, lies the indispensable tool of a personalized budget. A budget is far more than just a dry accounting ledger; it serves as a dynamic roadmap, meticulously planning your finances and providing clear insight into where every dollar of your money goes. Whether you are diligently working to make ends meet or fortunate enough to have extra income and aiming to refine your saving goals, budgeting is a powerful mechanism that empowers you to take control.

Creating a budget allows you to clearly visualize your financial inflows and outflows, revealing spending patterns that might otherwise remain hidden. This clarity is the first step toward identifying areas where you might be able to spend money differently, thereby freeing up valuable resources. The objective is twofold: first, to staunch the bleeding by stopping the accumulation of new debt, and second, to actively allocate funds toward paying down the debt you already carry, if your financial situation allows.

To construct your personalized budget, begin by gathering all relevant financial documents. This includes your bills for utilities, insurance, and other regular expenses, along with your pay stubs to accurately account for your income. Next, collect receipts or review bank statements for typical expenditures such as groceries, entertainment, transportation, clothing, and other everyday costs. This detailed collection process ensures that no expense category is overlooked, providing a truly comprehensive snapshot of your financial habits.

Once you have compiled this information, the process is straightforward: add up all of your paychecks and any other sources of income, then subtract your total expenses from that sum. The resulting figure will show you your net financial position for the month. With this clear overview in hand, the real work begins. Scrutinize your budget for areas where you might be able to make adjustments. Perhaps there are subscription services you no longer use, or opportunities to reduce discretionary spending on dining out or entertainment. Every dollar saved through mindful adjustments can then be strategically redirected.

The ultimate goal of this budgeting exercise is to generate a surplus that can be dedicated to debt reduction. By consciously reallocating funds that might have otherwise been spent on non-essentials, you empower yourself to make consistent, impactful payments toward your outstanding debts. This deliberate financial planning not only helps you stop adding to your debt but accelerates your journey toward becoming debt-free. For further assistance and resources on creating and tweaking your budget, valuable information and worksheets are readily available online, at your public library, and in bookstores, providing a solid foundation for financial empowerment.

### Advanced Debt Relief Pathways: A Comprehensive Guide

Having established a solid foundation in understanding and managing common debt types, our journey now turns to more advanced strategies and pathways for comprehensive debt relief. These methods often come into play when initial efforts prove insufficient or when the sheer volume of debt demands a more structured, external approach. From direct negotiations with collectors to considering the ultimate step of bankruptcy, understanding these options is crucial. Importantly, we will also equip you with the knowledge to identify and steer clear of predatory debt relief scams that can exacerbate an already challenging situation.

Read more about: Home Refinancing 101: Your Essential Guide to Knowing When to Refinance — And When to Hold Off for Bigger Savings

8. **When Debt Goes to Collections: Your Rights and Recourse**Even with diligent efforts, debt can sometimes end up in collections, a daunting experience often involving persistent contact. It’s vital to remember you have rights and specific recourse when dealing with collection agencies. Ideally, communicate with your original creditor before the debt is sold, as they may be more amenable to a modified payment plan. However, if debt has moved to a collector, understanding how to interact is key.

Collectors are legally required to provide “validation information” about the debt, either during their initial call or in writing within five days. This must include the amount owed, the creditor’s name, and how to get the original creditor’s name. You can dispute the debt if you believe it’s incorrect, ensuring you verify its legitimacy.

You can also assert your right to stop collector contact by sending a written letter. While this doesn’t erase the debt, it offers relief from persistent calls. Collectors are prohibited from harassment, like threatening harm or using obscene language, and from making false claims, such as pretending to be an attorney or threatening arrest. They cannot collect unapproved fees or publicly reveal your debts.

A critical aspect is the “statute of limitations,” a limited period during which collectors can legally sue you, usually starting from your first missed payment. Once this period expires, the debt is “time-barred,” and collectors cannot sue. Inform the judge if sued for a time-barred debt. However, in some states, making a payment or even acknowledging the debt in writing can reset this clock, so exercise caution.

9. **Leveraging Professional Credit Counseling for Debt Management**For individuals overwhelmed by debt, a reputable credit counseling organization offers invaluable guidance and structured solutions. These non-profit agencies provide advice on money and debt management, assist in budgeting, and offer educational materials. Their counselors are certified professionals, ensuring informed and practical assistance.

Good credit counselors dedicate time to understanding your entire financial situation before proposing solutions, typically through an hour-long initial session with follow-up offers. They won’t promise instant fixes or demand significant upfront payments. Reputable organizations offer services locally, online, or by phone, often with low fees.

One primary tool a counselor might recommend after a detailed review is a Debt Management Plan (DMP). DMPs help repay unsecured debts like credit card, student loan, or medical bills by consolidating them into one manageable monthly payment. Under a DMP, the counselor develops a payment schedule with you and your creditors, who may agree to lower interest rates or waive fees.

With a DMP, you make a single monthly deposit to the counseling organization, which distributes funds to your creditors. While effective, DMPs require consistent, timely payments and can take 48 months or more. You might also agree not to use new credit. Before committing, confirm your creditors offer the modifications described, as DMPs aren’t suitable for everyone.

Read more about: Navigating Your Finances: A NerdWallet Guide to Understanding, Managing, and Conquering Debt

10. **Navigating Debt Settlement Programs: Risks and Rewards**Debt settlement programs offer a distinct approach to relief, typically for those with significant credit card debt. For-profit companies negotiate with creditors to accept a “settlement”—a lump sum less than you owe. During this, you’re usually encouraged to stop direct monthly payments, instead setting aside funds in a designated account for settlement.

Despite the appeal of paying less, these programs carry substantial risks. Creditors aren’t obligated to settle, and negotiations might fail, leading to more debt from late fees and interest. Stopping payments severely damages your credit and can trigger aggressive collections or lawsuits.

Federal regulations mandate upfront disclosure from settlement companies. This includes fees, conditions, service terms, estimated resolution time, and consequences of halting payments. Crucially, fees cannot be collected until a debt is successfully settled, and then only a proportionate part for each.

If engaged, your money may be in a special account managed by an independent third party; these funds and interest are yours and can be withdrawn without penalty. However, many find it hard to complete programs due to duration and discipline. Also, remember potential tax implications, as debt relief savings could be taxable income.

11. **Understanding Debt Consolidation Loans: A Unified Approach**Debt consolidation simplifies repayment by combining multiple existing debts into a single, more manageable loan with one monthly payment. This is attractive for those juggling various obligations, streamlining the process and potentially reducing overall interest burden.

Options include a personal debt consolidation loan from a bank or finance company, offering a fixed interest rate and set term. Homeowners might use a second mortgage or a home equity line of credit (HELOC), which are secured and often have lower rates due to collateral.

While simplifying finances, consolidation has considerations. Secured loans, especially home-backed ones, risk collateral loss if payments are missed. Most consolidation loans also have costs like interest and “points.” Thorough calculation of all associated costs is vital to ensure a true financial advantage.

Before pursuing consolidation, evaluate your spending habits. If underlying issues aren’t addressed, new debt might accumulate on top of the consolidated loan, worsening your financial position. Consolidation is a tool; its effectiveness relies on responsible financial behavior and a commitment to avoid new debt.

12. **Considering Bankruptcy: A Fresh Start, A Last Resort**Bankruptcy is a serious yet often necessary last resort for individuals facing insurmountable debt, offering a fresh start. Filing for personal bankruptcy results in a court-ordered discharge, formally releasing you from repaying certain debts, providing immense relief.

However, bankruptcy significantly impacts your credit history, with details remaining on reports for up to 10 years. This can hinder future credit, mortgages, insurance, or even employment. Despite drawbacks, for those truly trapped by unmanageable debt, it’s a vital pathway to financial stability.

The two main types are Chapter 7 and Chapter 13, both filed in federal court. Chapter 7, “straight bankruptcy,” involves liquidating non-exempt assets (luxury items, additional properties) by a court-appointed trustee. Exempt assets like cars, work tools, and basic furnishings are typically protected, though specifics vary by state.

Chapter 13 is for individuals with steady income wishing to keep property. The court approves a 3-5 year repayment plan, with regular payments to creditors. After all plan payments, remaining eligible debts are discharged. Both chapters can discharge unsecured debts (credit cards, medical bills) and halt foreclosures, repossessions, and collection activities.

Before filing, federal law requires credit counseling from a government-approved organization up to six months prior. This ensures exploration of alternatives. Note that certain debts—child support, alimony, fines, taxes, and most student loans (unless undue hardship proven)—are typically not erased by bankruptcy.

13. **Identifying and Avoiding Debt Relief Scams**In the challenging landscape of debt, unscrupulous companies prey on vulnerable individuals seeking relief. These “debt relief scams” promise quick fixes or guaranteed results, often for hefty upfront fees, ultimately worsening financial positions. Vigilance and informed decision-making are paramount.

A crucial red flag is any organization demanding upfront fees before providing services or settling debts. Legitimate debt settlement companies are legally prohibited from collecting fees until a debt is successfully settled. No reputable organization guarantees to settle all debts, promises fast loan forgiveness, or claims results from “new government programs.”

Be highly suspicious of companies enrolling you without a thorough review of your financial situation. Genuine counselors understand your income, expenses, and debt before recommending a tailored plan. Scammers rush clients, prioritizing fees over financial well-being.

Another common scam tactic is advising you to stop communicating with creditors without explaining serious consequences like late fees, interest, and lawsuits. While some legitimate programs involve halting direct payments, they are transparent about risks. Scammers may also falsely claim they can stop all debt collection calls and lawsuits.

To protect yourself, research any company online using terms like “complaint” or “review.” Check with your state attorney general and local consumer protection agency for complaints. Remember, you can often negotiate with creditors or access legitimate government-approved counseling services for free or low cost. Never pay for services you can do yourself, and verify legitimacy before sharing personal or financial information.

Read more about: Beyond the Orchard: How Sweeping Deportation Changes Are Reshaping America’s Workforce and Economy, Leaving Crops to Rot

Navigating the complexities of debt is a challenging journey, yet one filled with numerous pathways to financial freedom. From strategic negotiations and professional counseling to more drastic measures like debt settlement and bankruptcy, options exist to help individuals regain control. The key lies in informed decision-making, understanding each approach’s intricacies, and diligently protecting yourself from predatory scams. By embracing knowledge and proactive engagement, saving thousands in interest and achieving lasting financial peace of mind is not just a possibility, but a tangible goal within reach.